Living as a foreign resident in Japan introduces a complex web of banking fees and financial charges that can significantly impact your monthly budget and long-term financial health. The Japanese banking system, while secure and reliable, operates under different principles than many international banking systems, creating unexpected costs and administrative burdens that catch many newcomers off guard during their initial months of residence.

The accumulation of banking fees represents one of the most overlooked expenses in budgeting for life in Japan, particularly for sharehouse residents who must navigate frequent money transfers, currency exchanges, and account maintenance charges. Understanding these costs and developing strategies to minimize them becomes essential for maintaining financial stability and maximizing your disposable income for housing, entertainment, and savings goals.

The Hidden Structure of Japanese Banking Costs

Japanese banks operate under a fee structure that differs fundamentally from banking systems in many Western countries, where basic services are often provided at minimal or no cost to account holders. The itemized charging system in Japan means that virtually every transaction, service request, and account activity generates specific fees that compound throughout each month to create substantial financial burdens for active account users.

Understanding living costs in Tokyo sharehouses becomes crucial when factoring in these additional banking expenses that can add hundreds of yen to your monthly obligations. The fee structure encompasses everything from basic ATM withdrawals during certain hours to international wire transfers, account maintenance charges, and currency conversion fees that apply to various financial activities.

Monthly account maintenance fees range from free basic accounts with limited services to premium accounts charging several hundred yen monthly for enhanced features and reduced transaction fees. The complexity arises from understanding which services justify these monthly charges versus the cumulative cost of individual transaction fees for users with varying banking activity levels.

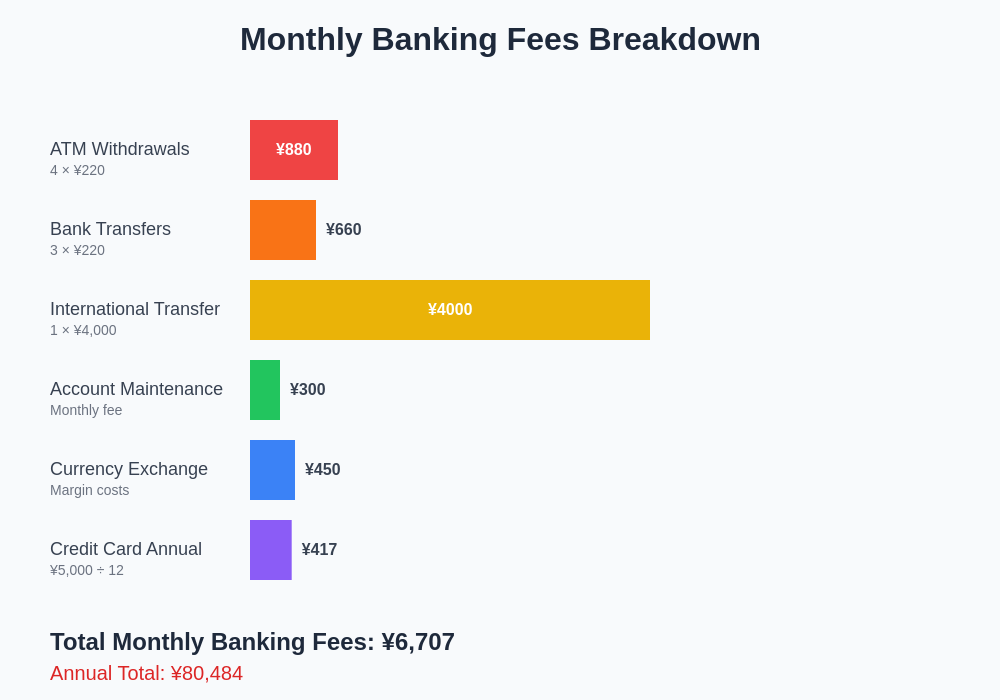

Transaction fees apply to numerous daily banking activities including ATM withdrawals outside your bank’s network, transfers between accounts at different banks, and even transfers between accounts within the same banking institution during certain time periods. These fees typically range from 110 to 330 yen per transaction, creating significant monthly expenses for residents who frequently move money between accounts or access cash from convenient locations.

ATM Network Complexities and Associated Costs

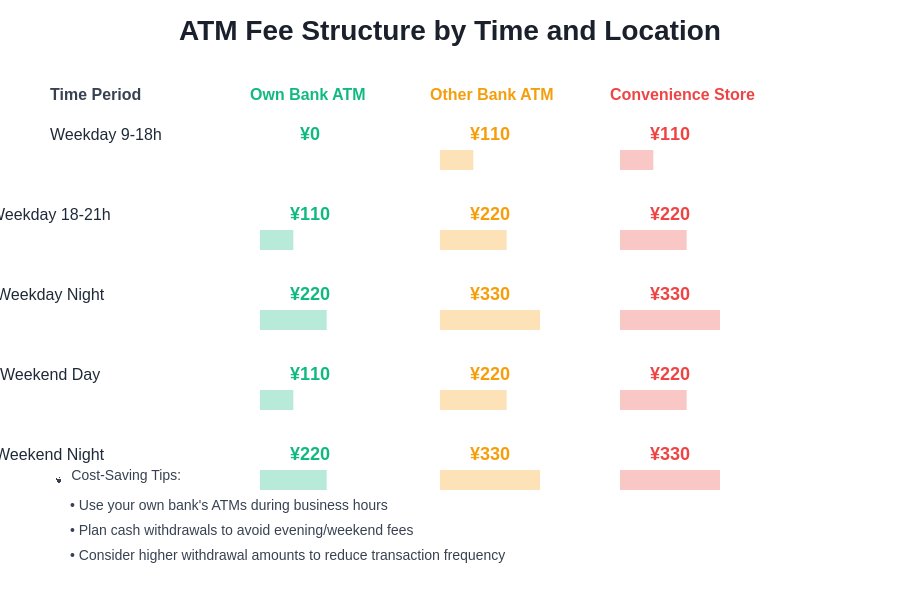

The Japanese ATM system operates under a network structure that creates variable costs depending on the time of day, day of the week, and specific ATM location where transactions occur. Understanding these patterns becomes essential for minimizing withdrawal fees that can easily accumulate to thousands of yen monthly for residents who frequently access cash for daily expenses and sharehouse payments.

Banking requirements for sharehouse applications often necessitate maintaining Japanese bank accounts that provide easy access to cash for rent payments and household expenses. The convenience of accessing money through numerous ATM locations comes with time-sensitive fee structures that penalize users for withdrawals during evenings, weekends, and holidays when surcharges can double or triple standard transaction costs.

Bank-specific ATMs typically offer the most favorable fee structures for account holders, with many major banks providing free withdrawals during standard business hours from their proprietary machines. However, the geographic distribution of these ATMs may not align with your daily routes or sharehouse location, forcing reliance on convenience store ATMs or partner bank machines that impose additional charges for access convenience.

Convenience store ATMs, while offering unparalleled accessibility throughout Japan, operate under premium fee structures that charge both the convenience store network and your originating bank for transaction processing. These combined fees often result in charges ranging from 110 to 220 yen per withdrawal, making frequent small withdrawals particularly expensive compared to less frequent larger cash access strategies.

International Transfer Fees and Currency Exchange Costs

Foreign residents frequently require international money transfer services for receiving funds from home countries, sending money to family abroad, or managing financial obligations that span multiple currencies. Japanese banks impose substantial fees for international wire transfers, with charges often ranging from 2,000 to 6,000 yen per transaction plus percentage-based fees calculated on the transfer amount.

Managing sharehouse payments and deposits often requires understanding how international transfers affect your ability to meet rental obligations and security deposit requirements. The timing of international transfers can impact your ability to secure housing, as processing delays combined with high fees may affect your capacity to provide required upfront payments when needed.

Currency exchange rates applied by Japanese banks typically include margins that favor the institution over the customer, resulting in exchange rate losses that compound the explicit transfer fees charged for international transactions. These margins can represent an additional 2-4% cost beyond posted exchange rates, creating hidden expenses that significantly impact the actual value of transferred funds.

Alternative transfer services such as online remittance companies and digital payment platforms often provide more favorable exchange rates and lower explicit fees compared to traditional Japanese banking channels. However, these services may require additional setup time, verification procedures, and integration with your Japanese banking accounts that create complexity during the initial establishment period.

Account Maintenance and Service Charges

Japanese banks impose various account maintenance charges that operate independently of transaction-based fees, creating ongoing monthly expenses that continue regardless of account activity levels. These charges encompass basic account maintenance fees, statement delivery charges, online banking service fees, and premium service subscriptions that enhance account functionality while increasing monthly costs.

Basic account maintenance typically ranges from zero cost for minimal service accounts to several hundred yen monthly for accounts that include enhanced ATM access, reduced transaction fees, or additional banking services. The decision between fee structures requires careful analysis of your banking activity patterns and cost-benefit evaluation of premium services versus individual transaction charges.

Statement delivery fees apply to both physical and electronic statement services, with many banks charging monthly fees for providing detailed transaction records and account summaries. Understanding utility bill management in sharehouses becomes relevant when considering how banking statement costs contribute to your overall record-keeping expenses for tax and budget management purposes.

Online banking services often require separate subscription fees beyond basic account maintenance, particularly for enhanced features such as mobile app access, detailed transaction categorization, and integration with personal finance management tools. These services, while convenient, represent additional monthly costs that accumulate over time and may exceed the value provided for users with simple banking needs.

Credit Card and Loan-Related Banking Fees

Foreign residents seeking to establish credit relationships with Japanese banks encounter additional fee structures related to credit card applications, loan origination charges, and ongoing credit maintenance costs. Credit card annual fees in Japan typically range from free basic cards to several thousand yen annually for premium reward cards, with foreign residents often limited to higher-fee options during their initial credit establishment period.

Sharehouse application processes and credit requirements may necessitate establishing credit relationships that involve ongoing fees for maintaining credit card accounts, even when balances remain paid in full monthly. These annual fees contribute to your overall banking costs while providing essential services for building credit history and accessing certain rental properties.

Loan application fees, processing charges, and ongoing loan maintenance costs create additional banking expenses for foreign residents seeking personal loans, auto financing, or other credit products. Even unsuccessful loan applications may result in processing fees and credit inquiry charges that impact your banking relationship costs without providing access to requested credit facilities.

Cash advance fees and foreign transaction charges on Japanese credit cards often exceed international standards, creating expensive options for accessing emergency funds or making purchases in foreign currencies during travel. Understanding these fee structures becomes important for foreign residents who maintain financial relationships with both Japanese and home country institutions.

Strategic Approaches to Minimizing Banking Costs

Developing effective strategies for minimizing banking fees requires understanding your personal financial patterns, banking activity requirements, and long-term residence plans in Japan. Budget planning for sharehouse living should incorporate banking fee projections based on your expected transaction frequency and service requirements.

Consolidating banking relationships with single institutions often provides opportunities for fee reductions through package deals, relationship pricing, and volume discounts that reward customers who maintain multiple accounts or services with the same bank. These relationships may offer reduced transaction fees, waived maintenance charges, or premium services at lower costs compared to maintaining scattered banking relationships.

Timing strategies for ATM usage, international transfers, and account activities can significantly reduce fee exposure by avoiding premium-rate time periods and utilizing favorable fee windows offered by your banking institutions. Understanding the specific fee schedules and optimal timing for your banking activities creates opportunities for substantial cost savings without reducing service quality or access convenience.

Managing financial obligations in sharehouses benefits from banking strategies that minimize transaction costs while maintaining necessary access to funds for rent payments, utility bills, and household expenses. Coordinating payment schedules and cash access patterns with favorable banking fee structures optimizes your monthly financial efficiency.

Digital Banking Alternatives and Cost Comparisons

The emergence of digital banking platforms and online financial services in Japan provides alternative approaches to traditional banking relationships, often with different fee structures that may benefit foreign residents with specific banking activity patterns. These platforms typically offer reduced overhead costs and streamlined service delivery that can translate into lower fees for users who primarily conduct banking activities through digital channels.

Cryptocurrency and digital payment platforms create alternative methods for international transfers and currency exchange that may offer competitive rates compared to traditional banking channels. However, these alternatives require careful evaluation of regulatory compliance, tax implications, and integration with your overall financial management strategy in Japan.

Understanding payment methods in sharehouse living helps evaluate how digital banking alternatives integrate with rental payment requirements and household expense management. Some sharehouses and service providers may not accept digital payment methods, limiting the practical benefits of alternative banking solutions.

Comparison shopping between traditional banks, online banks, and hybrid financial services reveals significant variations in fee structures, service offerings, and total cost of ownership for banking relationships. Regular evaluation of your banking costs versus available alternatives ensures you maintain optimal financial efficiency as your residence status and banking needs evolve.

Tax Implications and Record-Keeping Costs

Banking fees themselves may qualify for tax deductions or business expense classifications depending on your employment status, visa category, and income sources in Japan. Managing documentation for sharehouse living extends to maintaining banking records that support tax compliance and expense tracking for potential deductions.

The cost of obtaining detailed banking records, transaction histories, and account summaries for tax preparation purposes represents additional banking-related expenses that accumulate annually. Many banks charge fees for providing historical records, certified statements, and documentation required for tax filing or visa renewal processes.

Record-keeping services and account management tools offered by banks often involve subscription fees that contribute to your overall banking costs while providing organization and tracking benefits for personal financial management. Evaluating the cost-effectiveness of these services versus manual record-keeping approaches helps optimize your total banking expense structure.

Planning for Long-Term Banking Relationships

Establishing sustainable banking relationships as a foreign resident requires considering the long-term cost implications of various fee structures and service levels as your residence status, income, and financial needs evolve over time. Building financial stability in sharehouse communities may benefit from banking relationships that support both immediate needs and future financial growth opportunities.

Relationship banking strategies that involve maintaining higher account balances, utilizing multiple services, or committing to longer-term banking relationships often provide fee reductions and enhanced service levels that justify initial costs through long-term savings and improved banking experiences. Evaluating these opportunities requires careful analysis of your financial capacity and residence plans.

Building credit history and establishing financial credibility with Japanese banking institutions creates long-term value that may justify higher initial banking costs in exchange for access to better loan rates, reduced fees, and enhanced financial product availability. Long-term financial planning for international residents benefits from strategic banking relationship development that supports broader financial goals.

The accumulation of banking fees for foreign residents in Japan represents a significant but manageable financial challenge that requires awareness, strategic planning, and ongoing optimization to minimize impact on your overall budget and financial goals. Understanding the fee structures, developing cost-minimization strategies, and maintaining flexibility in your banking relationships creates opportunities to reduce these expenses while maintaining necessary financial services for successful life in Japan. Through careful planning and informed decision-making, banking fees can be controlled and integrated into your overall financial strategy without compromising your quality of life or long-term financial objectives.

Disclaimer

This article is for informational purposes only and does not constitute professional financial advice. Banking fees, regulations, and service offerings change frequently, and individual circumstances may affect the applicability of strategies discussed. Readers should consult with qualified financial professionals and verify current fee structures with specific banking institutions before making financial decisions. The effectiveness of cost-minimization strategies may vary based on personal banking patterns, residence status, and individual financial goals.