Insurance claims in Japanese sharehouses present a labyrinthine array of complications that can transform seemingly straightforward incidents into months-long disputes involving multiple parties, conflicting policies, and complex legal interpretations. The shared nature of these living arrangements creates unique scenarios where determining liability, establishing coverage, and processing claims becomes exponentially more difficult than traditional single-tenant situations.

The intersection of Japanese insurance regulations, sharehouse management structures, and international resident rights creates a perfect storm of bureaucratic complexity that often leaves residents financially vulnerable when accidents occur. Understanding these complications before they arise can mean the difference between swift resolution and prolonged financial hardship during your most challenging moments.

The Multi-Party Liability Maze

Insurance claims in sharehouses become exponentially more complex due to the involvement of multiple potential liability sources, each with their own insurance policies, legal obligations, and incentives to minimize their financial responsibility. Understanding what security deposits actually cover in sharehouses reveals how property damage costs often fall outside standard deposit protections, forcing residents into the insurance system.

When property damage occurs in a sharehouse, determining the responsible party requires investigation into whether the damage resulted from individual negligence, building maintenance failures, or shared facility malfunctions. Property management companies, building owners, individual residents, and utility companies may all become involved in liability disputes, each with different insurance coverage levels and claim processing procedures.

The complexity multiplies when damage affects both private rooms and common areas, creating jurisdictional disputes between different insurance policies that may have conflicting definitions of coverage boundaries. A single water leak, for example, might involve the building’s structural insurance, the management company’s liability coverage, and individual residents’ personal property protection, with each insurer potentially disputing their obligation to cover specific damages.

Japanese insurance law requires clear establishment of causation and negligence, but sharehouse environments make these determinations incredibly difficult when multiple residents have access to the same facilities and systems. The burden of proof often falls on claimants to demonstrate specific responsibility, creating situations where legitimate claims are denied due to insufficient evidence rather than lack of actual coverage.

Documentation and Evidence Challenges

The shared nature of sharehouse living creates unique obstacles for gathering the comprehensive documentation required for successful insurance claims in Japan. How to actually get your deposit back demonstrates how thorough documentation affects financial outcomes, principles that apply equally to insurance situations.

Photographic evidence becomes problematic when damage occurs in shared spaces where multiple residents have legitimate access, making it difficult to establish timelines and causation that insurance companies require for claim validation. Security camera footage, when available, often has limited retention periods or inadequate coverage angles that fail to capture the specific incidents that lead to damage claims.

Witness statements from other residents may be compromised by language barriers, cultural differences in observational reporting, or reluctance to implicate housemates in potentially expensive liability situations. The transient nature of sharehouse populations means that key witnesses may have moved out by the time claims are processed, leaving gaps in testimony that insurers exploit to deny coverage.

Medical documentation for personal injury claims becomes complicated when Japanese healthcare providers are unfamiliar with foreign insurance requirements or when language barriers prevent accurate communication of symptoms and treatment needs. The integration between Japanese national health insurance and private property insurance creates additional layers of documentation requirements that many residents are unprepared to navigate.

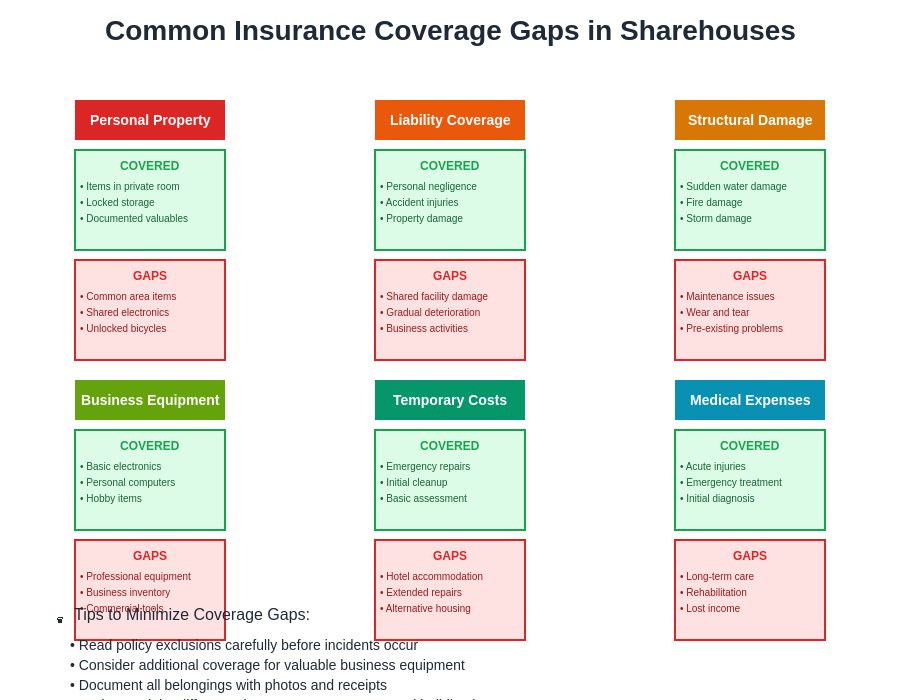

Coverage Gap Complications

Standard sharehouse insurance arrangements often contain significant coverage gaps that only become apparent when claims are filed, leaving residents financially responsible for damages they assumed were covered. Why sharehouse insurance matters more than you think explores these hidden vulnerabilities that can result in substantial unexpected expenses.

Personal property coverage in shared living situations frequently excludes items stored in common areas or shared refrigerators, creating disputes about where damage occurred and whether coverage applies. Electronics, bicycles, and other valuable items that residents commonly store in shared spaces may not receive protection under standard policies, despite residents’ reasonable expectations of coverage.

Liability coverage often contains exclusions for damage caused by “normal wear and tear” or “gradual deterioration,” but these terms are interpreted differently by various insurance companies and may not align with residents’ understanding of covered events. What appears to be sudden damage may be classified as gradual deterioration if underlying maintenance issues contributed to the incident.

Business-related property receives limited or no coverage under residential policies, affecting residents who work from home or operate small businesses from their sharehouse rooms. The increasing prevalence of remote work has created new categories of uncovered property that many residents discover only after expensive equipment is damaged or stolen.

Language and Cultural Barriers

Insurance claim processing in Japan involves substantial paperwork, phone conversations, and in-person meetings conducted primarily in Japanese, creating significant barriers for international residents who may lack the specific vocabulary needed to describe damage, explain circumstances, or understand policy terms. Japanese sharehouse rules every foreigner should know includes insurance-related obligations that foreign residents often misunderstand.

Technical insurance terminology translates poorly between languages, leading to misunderstandings about coverage scope, deductible amounts, and claim procedures that can result in inadvertent policy violations or missed deadlines. Professional translation services add costs and delays to claim processing, while relying on friends or online translation tools may introduce errors that compromise claim validity.

Cultural differences in communication styles affect claim presentations, with Japanese insurance adjusters expecting specific levels of formality, detail, and procedural compliance that may not be intuitive to international residents. Direct confrontation or aggressive advocacy, common in Western insurance interactions, can be counterproductive in Japanese business culture and may harm claim prospects.

The concept of shared responsibility, deeply embedded in Japanese society, influences how insurance companies evaluate sharehouse claims and may result in partial liability assignments that differ from residents’ expectations of full coverage for covered events.

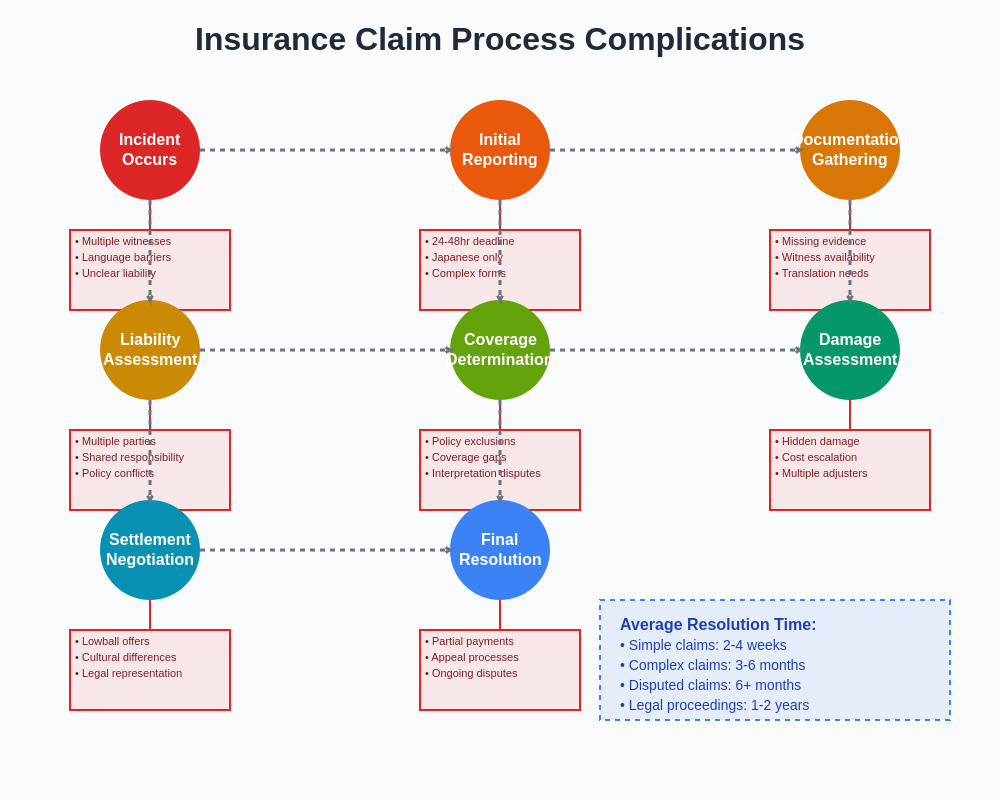

Timing and Procedural Complexities

Japanese insurance companies impose strict notification timelines that can be as short as 24-48 hours for certain types of claims, but sharehouse residents often lack awareness of these requirements until it’s too late to comply. How to handle roommate conflicts without moving out reveals communication challenges that extend to insurance reporting obligations.

Weekend and holiday reporting requirements create additional complications when damage occurs during non-business hours, as many insurance companies do not accept emergency notifications through automated systems and require direct communication with claims representatives. The Golden Week holiday period and other extended Japanese holidays can delay claim initiation by weeks, potentially affecting coverage eligibility.

Multiple insurance policies with different claim procedures must be coordinated when damage affects both individual property and shared facilities, requiring residents to navigate potentially contradictory requirements and timelines simultaneously. Missing any single procedural requirement can invalidate entire claims, regardless of coverage validity.

The appeals process for denied claims involves additional layers of bureaucracy and timing requirements that many residents are unprepared to navigate, particularly when dealing with Japanese legal concepts and procedures that have no direct equivalents in other countries’ insurance systems.

Financial Impact Escalation

Initial damage assessments frequently underestimate total costs, particularly when structural issues or hidden damage emerges during repair processes, but insurance coverage determinations are often based on preliminary estimates that may not reflect final expenses. Living costs in Tokyo sharehouses explained shows how unexpected expenses can devastate carefully planned budgets.

Temporary accommodation costs during major repairs can exceed insurance allowances, leaving residents responsible for hotel bills or alternative housing expenses that may continue for weeks or months while repairs are completed. The limited availability of temporary furnished accommodations in Tokyo drives up costs beyond typical insurance coverage limits.

Legal fees for disputed claims can quickly exceed the value of the original damage, creating situations where residents must choose between accepting unfavorable settlements and pursuing expensive legal remedies that may not guarantee better outcomes. The Japanese legal system’s emphasis on mediation and compromise may not align with residents’ expectations of full compensation.

Currency exchange rate fluctuations affect international residents whose income is in foreign currencies, making it difficult to budget for deductibles, legal fees, and uncovered expenses when claims processing extends over several months and exchange rates shift significantly.

This timeline demonstrates how a seemingly minor incident can evolve into a major financial burden through various complications and delays that are common in sharehouse insurance situations.

Inter-Resident Liability Disputes

When one resident’s actions cause damage that affects other residents’ property or living situations, insurance claims become complicated by competing interests and potential counter-claims between housemates. How cleaning responsibilities create house drama illustrates how daily conflicts can escalate into serious liability issues.

Subrogation rights allow insurance companies to pursue recovery from responsible parties even after paying claims, potentially creating ongoing legal obligations between former housemates long after the original incident occurred. Residents may find themselves defendants in lawsuits filed by insurance companies seeking recovery for claims they paid to other residents.

Joint and several liability principles in Japanese law can make all residents potentially responsible for damages caused by any individual resident when shared facilities or common areas are involved, regardless of direct participation in the damaging incident. This legal concept often surprises international residents who expect individual responsibility for individual actions.

Shared utility insurance claims, such as those involving electrical systems or plumbing failures, may require all affected residents to coordinate their individual claims and potentially share liability for damages, creating conflicts when residents have different insurance coverage levels or deductible amounts.

Management Company Involvement

Sharehouse management companies often serve as intermediaries in insurance claims but may have conflicting interests that prioritize property protection over resident compensation, leading to delayed or inadequately processed claims. Why some sharehouses charge hidden cleaning fees demonstrates how management priorities can conflict with resident interests.

Property managers may lack adequate insurance knowledge or authority to make binding commitments during claim discussions, resulting in miscommunications and false expectations that become problematic when formal claim decisions are made by insurance companies. Residents often receive informal assurances from management staff that are not honored by actual insurance policies.

Conflict of interest situations arise when management companies have financial incentives to minimize insurance claims to maintain favorable relationships with insurance providers, potentially resulting in inadequate advocacy for residents’ legitimate claims. Some management companies receive benefits or preferential rates for maintaining low claim frequencies.

The quality and responsiveness of management company insurance support varies dramatically between operators, with some providing comprehensive assistance while others offer minimal help, leaving residents to navigate complex claim processes independently despite paying management fees that theoretically include such services.

Preventive Documentation Strategies

Creating comprehensive photographic records of personal property and room conditions upon move-in provides essential baseline documentation that can support future insurance claims when damage occurs. What documents you need for Tokyo sharehouse applications emphasizes documentation importance that extends throughout residency.

Regular communication logs with management companies, including email records of maintenance requests and facility problems, establish timelines and notice provisions that can be crucial for demonstrating proper procedures were followed when claims arise. Written documentation carries more weight than verbal communications in Japanese legal and insurance contexts.

Maintaining inventory lists with photographs, serial numbers, and purchase receipts for valuable items enables faster and more accurate claim processing when theft or damage occurs. Digital storage of these records in cloud services ensures availability even when physical documents are damaged in the same incident that triggers the insurance claim.

Understanding specific policy terms and exclusions before incidents occur allows residents to take appropriate precautions and maintain coverage eligibility through proper equipment maintenance, security measures, and facility usage that aligns with insurance requirements.

Professional Support Resources

Insurance claim assistance services, while adding cost to claim processing, can provide valuable expertise in navigating Japanese insurance procedures and ensuring proper documentation and presentation of claims. How to find the perfect sharehouse in Tokyo includes evaluation of support services that can benefit residents throughout their tenancy.

Legal consultation services specializing in tenant rights and insurance disputes can provide guidance on complex liability situations and help residents understand their options when facing denied or inadequately settled claims. Some legal insurance policies available to foreign residents include coverage for consultation and representation in insurance disputes.

Professional translation services ensure accurate communication with insurance companies and proper understanding of policy terms and claim requirements, potentially improving claim outcomes despite the additional expense. Many insurance companies provide limited English-language support that may not be adequate for complex claim situations.

Resident advocacy organizations and international community resources may provide assistance or referrals for insurance-related problems, particularly for residents who lack language skills or cultural knowledge needed to effectively navigate Japanese insurance systems independently.

The complexity of insurance claims in Japanese sharehouses requires proactive preparation, realistic expectations, and often professional assistance to achieve satisfactory outcomes. Understanding these complications before they arise enables better decision-making about insurance coverage, documentation practices, and response strategies that can minimize financial impact and stress during already challenging situations. The investment in comprehensive insurance understanding and professional support often pays dividends when unexpected incidents occur in shared living environments.

Disclaimer

This article is for informational purposes only and does not constitute professional legal or insurance advice. Insurance policies and claim procedures vary significantly between companies and specific situations. Readers should consult with qualified insurance professionals and legal advisors for guidance on their specific circumstances. The information provided reflects general patterns and experiences but may not apply to all situations or insurance products available in Japan.