The banking and payment requirements for Tokyo sharehouses create a complex landscape that often confuses international residents attempting to secure accommodation in Japan’s capital city. Understanding why these requirements vary so dramatically between different properties and management companies becomes essential for successfully navigating the application process and avoiding costly delays or rejections that can derail your housing search entirely.

The variation in bank account requirements stems from multiple interconnected factors including risk management policies, administrative efficiency considerations, legal compliance requirements, and the specific business models employed by different sharehouse operators. These requirements can range from mandatory Japanese bank accounts with automatic debit authorization to flexible international payment options that accommodate various financial situations and visa statuses.

The Foundation of Payment System Complexity

Japanese sharehouses operate within a highly regulated financial environment where payment processing, tenant verification, and risk management intersect to create diverse requirement structures across different operators and property types. How to find the perfect sharehouse in Tokyo becomes significantly more complex when banking requirements add additional layers to the application process.

The fundamental challenge lies in balancing accessibility for international residents against operational efficiency and financial security for property management companies. Large-scale operators often implement standardized systems that prioritize automation and cost reduction, while smaller independent sharehouses may offer more flexible arrangements that accommodate individual circumstances but require more manual processing and oversight.

Traditional Japanese banking practices emphasize stability, long-term relationships, and comprehensive documentation, creating inherent conflicts with the transient nature of international sharehouse residents who may have temporary visa status, limited credit history, or complex income sources that don’t align with standard banking verification procedures.

Risk Assessment and Management Strategies

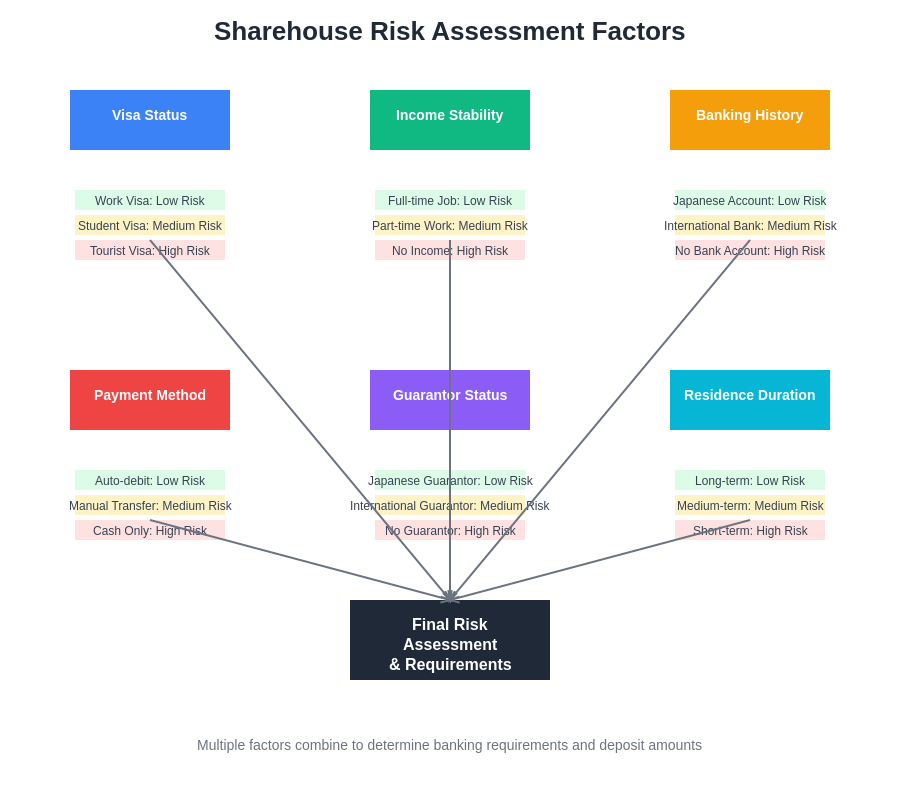

Different sharehouse operators employ varying risk assessment methodologies that directly influence their banking and payment requirements, with some prioritizing comprehensive financial verification while others focus on alternative security measures such as larger deposits or guarantor arrangements. Understanding utility bills in Japanese sharehouses often connects to these payment systems and risk management approaches.

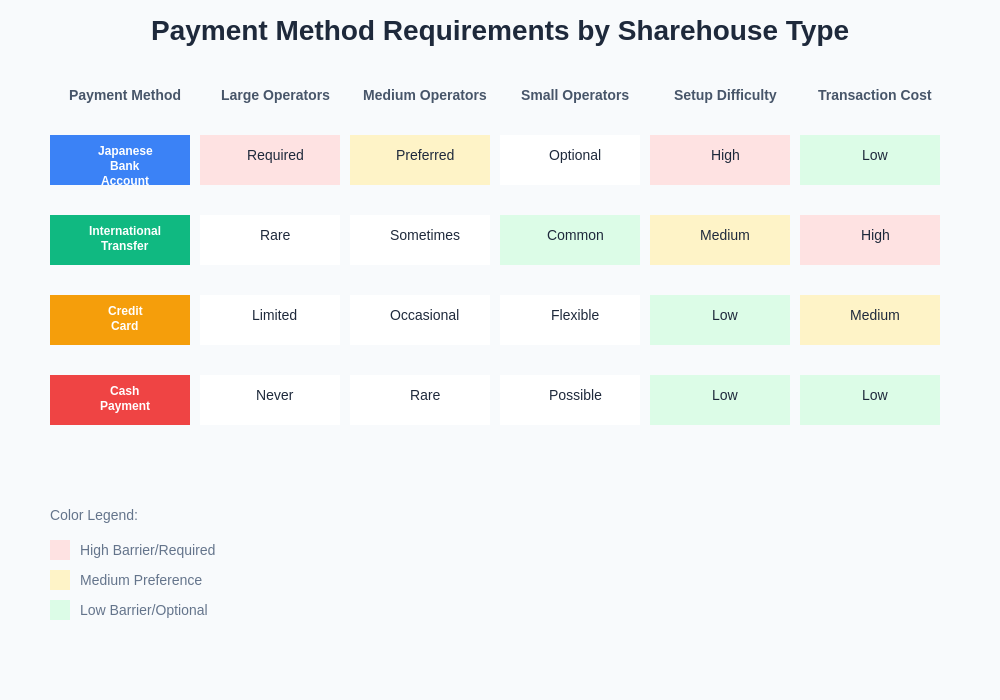

Large corporate operators typically implement automated payment systems that require Japanese bank accounts with direct debit capabilities, enabling efficient rent collection while minimizing administrative overhead and reducing the risk of payment delays or defaults. These systems often integrate with comprehensive tenant management platforms that track payment history, automate late fee calculations, and generate detailed financial reports for property owners and investors.

Smaller operators may accept international bank transfers, credit card payments, or even cash arrangements, but these flexible options often come with higher administrative costs that get passed on to residents through increased fees, stricter deposit requirements, or more frequent payment schedules that ensure cash flow stability despite less predictable payment methods.

The perceived risk associated with different visa types significantly influences banking requirements, with work visa holders often facing fewer restrictions than student visa holders or working holiday participants, whose temporary status and potentially irregular income streams create additional uncertainty for property managers seeking reliable long-term tenants.

Operational Efficiency and Administrative Considerations

The administrative burden associated with different payment methods creates significant cost variations that influence which options sharehouses choose to offer, with automated Japanese bank account systems providing the lowest ongoing management costs while international payment methods require manual processing, currency conversion management, and additional verification procedures.

Japanese sharehouse rules every foreigner should know often include specific payment protocols that reflect these operational considerations and help residents understand why certain requirements exist beyond simple preference or convenience factors.

Automated direct debit systems enable sharehouses to process hundreds of payments simultaneously on specific dates each month, reducing staff time, minimizing errors, and providing predictable cash flow that supports operational planning and financial forecasting. These systems also automatically generate payment confirmations, late payment notifications, and detailed transaction records that satisfy accounting and tax requirements.

Manual payment processing requires dedicated staff time for each transaction, involves higher error rates, creates delays in payment confirmation, and often necessitates additional communication with residents to resolve issues or provide payment confirmations. These factors significantly increase operational costs that must be absorbed by the business or passed on to residents through higher fees or stricter requirements.

Legal and Regulatory Compliance Factors

Japanese financial regulations impose specific requirements on businesses that collect recurring payments, manage security deposits, and process international transactions, creating compliance obligations that vary significantly based on the payment methods and banking arrangements employed by different sharehouse operators.

Anti-money laundering regulations require comprehensive identity verification and transaction monitoring for certain types of payments, particularly those involving international transfers or cash transactions above specific thresholds. These requirements create additional administrative burdens that some operators choose to avoid by restricting payment methods to those with simplified compliance procedures.

Consumer protection laws mandate specific disclosure requirements, dispute resolution procedures, and refund processes that become more complex when multiple payment methods are involved. Sharehouses must maintain detailed records, provide standardized documentation, and ensure that all payment processing meets regulatory standards regardless of the specific methods employed.

How to actually get your deposit back often depends on understanding these regulatory frameworks and ensuring that your payment arrangements comply with all applicable laws and regulations that protect both tenants and property managers.

Technology Infrastructure and Integration Capabilities

The technological infrastructure available to different sharehouse operators creates significant variations in their ability to support diverse payment methods, with larger companies investing in comprehensive systems while smaller operators may rely on basic banking services that limit their payment options and create different requirement structures.

Modern payment processing platforms enable integration with multiple banks, support various currencies, provide real-time transaction monitoring, and offer automated reconciliation features that reduce administrative overhead while maintaining detailed audit trails. However, these sophisticated systems require significant upfront investment and ongoing maintenance costs that smaller operators may not be able to justify.

Basic banking arrangements through traditional Japanese financial institutions often provide limited payment options, require manual processing for international transactions, and offer minimal integration capabilities with property management systems. These limitations force operators to implement more restrictive requirements that ensure compatibility with their available infrastructure.

Living costs in Tokyo sharehouses explained includes understanding how payment system limitations can affect overall monthly expenses through additional fees, currency conversion costs, or required banking services that add to the total cost of residence.

International Resident Accommodation Strategies

Sharehouses that specifically target international residents often develop specialized payment systems and banking requirements that accommodate the unique challenges faced by foreign residents, including limited credit history, temporary visa status, and unfamiliarity with Japanese banking procedures and cultural expectations.

English-speaking sharehouses in Tokyo for foreigners frequently offer alternative payment arrangements such as international bank transfers, online payment platforms, or partnerships with specific banks that provide streamlined account opening procedures for international residents with proper visa documentation.

These accommodations often come with additional costs or requirements such as higher security deposits, more frequent payment schedules, or mandatory financial guarantees that compensate for the increased administrative complexity and perceived risk associated with international payment methods and temporary resident status.

Some operators partner with international money transfer services, digital payment platforms, or specialized banks that cater to foreign residents, creating integrated solutions that simplify the payment process while maintaining compliance with Japanese regulations and providing adequate security for property managers and owners.

Visa Status and Financial Verification Requirements

Different visa categories carry varying levels of perceived stability and financial reliability, directly influencing the banking requirements imposed by sharehouse operators who assess risk based on residency status, employment authorization, and the likelihood of payment continuity throughout the lease period.

Work visa holders typically face the least restrictive banking requirements due to their stable employment status, longer-term residency prospects, and established income streams that provide confidence in their ability to maintain consistent payments throughout their tenancy period. Student sharehouses near top Tokyo universities often have different requirements reflecting the unique circumstances of academic residents.

Student visa holders may encounter more complex requirements due to potential income limitations, dependence on family support, and uncertain post-graduation plans that create questions about long-term payment reliability. Some operators require additional guarantees, more frequent payment schedules, or specific banking arrangements that provide enhanced security for student residents.

Working holiday visa participants often face the most restrictive requirements due to their temporary status, potential employment gaps, and likelihood of departure before lease completion. These factors may result in requirements for upfront payments, international guarantees, or specific banking arrangements that minimize risk while accommodating the transient nature of working holiday experiences.

Property Management Company Size and Business Models

Large corporate sharehouse operators typically implement standardized policies across their entire portfolio, creating consistent but potentially inflexible requirements that prioritize operational efficiency over individual accommodation but provide predictable application processes and clear requirements for prospective residents.

These operators often invest in sophisticated payment processing systems, automated rent collection, and integrated property management platforms that enable them to offer competitive pricing through operational efficiencies but may limit payment options to those that integrate seamlessly with their chosen technology infrastructure.

Best sharehouses in Tokyo often represent these larger operators who can provide comprehensive services, professional management, and standardized procedures, but their banking requirements may be less flexible for residents with unique circumstances or preferences.

Smaller independent operators frequently offer more personalized service and flexible payment arrangements but may lack the technology infrastructure or administrative resources to support diverse payment methods efficiently. These operators might accept alternative arrangements on a case-by-case basis but often require additional security measures to compensate for increased administrative complexity.

Mid-sized operators often provide balanced approaches that combine some standardization with flexibility, offering multiple payment options while maintaining operational efficiency through selective technology investments and streamlined procedures that accommodate diverse resident needs without compromising business viability.

Geographic and Demographic Targeting Considerations

Sharehouses located in areas with high concentrations of international residents often develop payment systems specifically designed to accommodate foreign banking preferences and requirements, while properties in predominantly Japanese neighborhoods may maintain traditional banking requirements that reflect local customs and expectations.

Best Tokyo neighborhoods for sharehouse living often correlate with varying banking requirement approaches, as operators adjust their policies based on their target demographic and the competitive landscape in their specific market areas.

Properties near international universities, business districts with foreign companies, or tourist areas typically offer more flexible banking options to attract and retain international residents who may prefer familiar payment methods or face challenges opening Japanese bank accounts immediately upon arrival.

Suburban sharehouses may maintain more traditional Japanese banking requirements due to their local customer base, lower competition for international residents, and operational models that prioritize cost efficiency over accommodation of diverse payment preferences or international banking arrangements.

Currency and Exchange Rate Management

International payment methods introduce currency exchange rate risks and administrative complexities that different sharehouses handle through various approaches, from passing exchange costs directly to residents to absorbing these costs through higher base rates or requiring local currency payments to eliminate exchange rate exposure entirely.

Properties that accept international payments must develop procedures for handling exchange rate fluctuations, ensuring consistent rent collection despite currency volatility, and managing the administrative overhead associated with multiple currencies and international banking relationships that require specialized knowledge and ongoing management.

How commute times impact your quality of life becomes relevant when banking requirements affect location choices, as residents may need to balance proximity to specific banks or payment processing centers against other lifestyle and convenience factors.

Some operators establish partnerships with currency exchange services or international banks to provide residents with favorable exchange rates and simplified payment procedures, while others require residents to handle currency conversion independently, which can result in unpredictable monthly costs and administrative complications.

Deposit and Security Arrangement Variations

The banking requirements often correlate directly with deposit and security arrangement policies, as operators use different combinations of financial security measures to achieve their desired risk management objectives while accommodating various resident circumstances and payment capabilities.

Properties with restrictive banking requirements may offer lower deposit amounts or more flexible deposit payment schedules to compensate for the inconvenience and administrative burden imposed on residents who must establish specific banking relationships or payment arrangements to meet the property’s requirements.

What security deposits actually cover in sharehouses explains how these various financial arrangements work together to provide security for property managers while ensuring that residents understand their obligations and the protection provided by different payment and deposit structures.

Alternative security arrangements such as guarantor requirements, insurance products, or graduated deposit systems may be offered in conjunction with specific banking requirements, creating package arrangements that provide multiple layers of financial protection while accommodating residents with different banking capabilities and preferences.

Future Trends and Evolving Requirements

The sharehouse industry continues to evolve as technology advances, international resident populations grow, and regulatory frameworks adapt to changing demographics and business models, creating ongoing shifts in banking requirement approaches and payment system capabilities across the Tokyo market.

Digital payment platforms, cryptocurrency adoption, and international banking integration continue to expand the available options for sharehouses and residents, while regulatory changes and consumer protection enhancements may influence how different payment methods are implemented and managed by property operators.

Making friends through Tokyo sharehouse communities increasingly includes residents from diverse financial backgrounds and banking preferences, encouraging operators to develop more inclusive payment systems that accommodate international diversity while maintaining operational efficiency and financial security.

The competitive landscape continues to drive innovation in payment systems and banking requirements as operators seek to differentiate their properties and attract international residents through convenient, flexible, and transparent financial arrangements that reflect modern expectations while respecting traditional Japanese business practices.

Understanding the complex factors behind varying bank account requirements enables prospective residents to make informed decisions about which sharehouses align with their financial capabilities and preferences while preparing appropriate documentation and banking arrangements that facilitate smooth application processes and successful long-term residency experiences in Tokyo’s dynamic sharehouse market.

Disclaimer

This article is for informational purposes only and does not constitute professional financial or legal advice. Banking requirements and payment systems for sharehouses in Tokyo are subject to change, and specific requirements may vary significantly between operators and properties. Readers should verify current requirements directly with prospective sharehouses and consult with qualified professionals regarding banking and financial matters. The effectiveness of different payment strategies may vary depending on individual circumstances, visa status, and specific property requirements.