Exchange rate fluctuations represent one of the most unpredictable and potentially devastating financial challenges facing international residents living in Tokyo sharehouses. The relationship between your home currency and the Japanese yen directly influences every aspect of your monthly budget, from rent payments to daily living expenses, creating a complex web of financial uncertainty that can transform affordable living situations into unmanageable financial burdens within weeks or even days of market volatility.

The psychological stress and practical complications arising from currency volatility extend far beyond simple mathematical calculations, affecting housing decisions, career choices, and long-term life planning for thousands of international residents who must navigate the challenging intersection of global financial markets and personal budget management while pursuing their dreams in one of the world’s most expensive cities.

The Fundamental Nature of Currency Risk in Sharehouse Living

Currency risk in sharehouse living operates as a constant background force that influences every financial decision and long-term commitment made by international residents. Unlike domestic renters who enjoy stable, predictable monthly expenses denominated in their earning currency, international sharehouse residents face the daily reality that their purchasing power can change dramatically based on global economic events entirely outside their control or influence.

The structure of most sharehouse contracts requires payment in Japanese yen, creating immediate exposure to exchange rate movements for residents whose income arrives in foreign currencies. How much Tokyo sharehouses really cost per month becomes a moving target when your home currency weakens against the yen, potentially increasing your effective housing costs by twenty or thirty percent without any change in your actual living situation or housing quality.

This currency exposure compounds over time, affecting not only immediate monthly expenses but also long-term financial planning, emergency fund adequacy, and the ability to maintain consistent living standards throughout extended periods of residence. The psychological burden of constant financial uncertainty can impact academic performance, career development, and overall quality of life for residents who struggle to establish stable budgetary frameworks in volatile currency environments.

Direct Impact on Monthly Housing Expenses

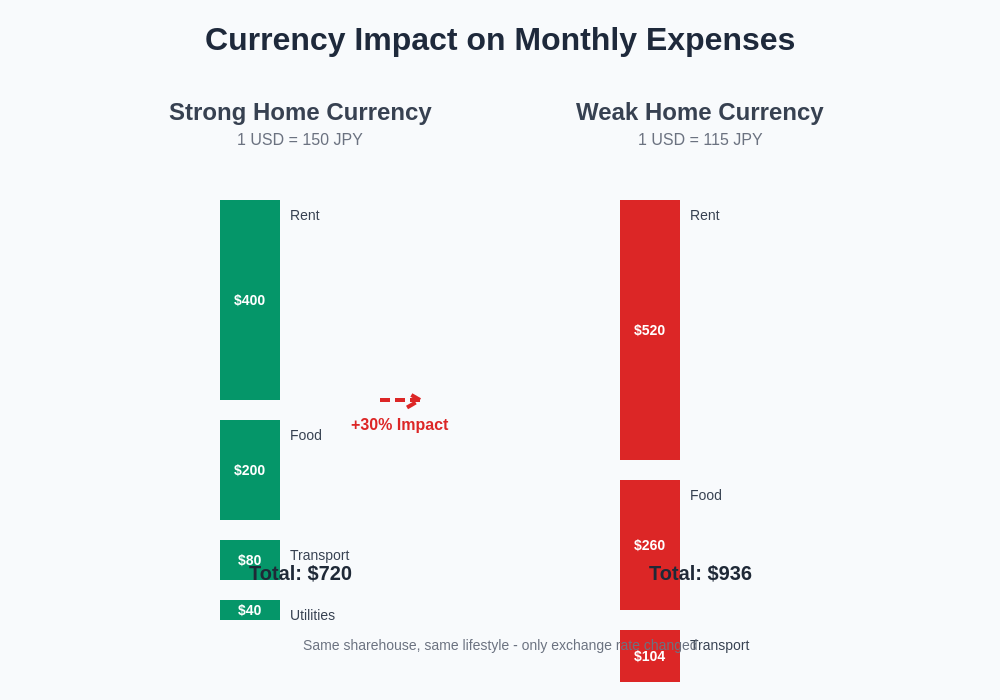

Monthly housing expenses represent the largest and most predictable component of sharehouse living costs, yet currency fluctuations can transform this seemingly stable expense into a source of ongoing financial stress and budget disruption. A sharehouse room costing ¥60,000 per month might represent entirely different financial commitments depending on whether your home currency is experiencing strength or weakness against the yen.

For American residents, periods when the dollar weakens from ¥150 to ¥130 per dollar increase the effective monthly rent from $400 to approximately $460, representing a fifteen percent increase in housing costs without any improvement in living conditions or services. European residents face similar challenges when the euro fluctuates against the yen, while residents from emerging market economies may experience even more dramatic swings that can double or halve their effective housing costs over relatively short periods.

The timing of currency movements relative to contract commitments creates additional complications, as residents may sign lease agreements during favorable exchange rate periods only to find themselves locked into financially unsustainable commitments when currencies move unfavorably. Contract terms that are more important than advertised prices become even more critical when currency risk amplifies the financial implications of inflexible lease arrangements.

The compounding effect of currency-driven rent increases affects every other aspect of monthly budgeting, reducing available funds for food, transportation, entertainment, and emergency savings while creating pressure to find additional income sources or reduce living standards to maintain financial stability.

Compound Effects on Daily Living Costs

Daily living expenses in Tokyo sharehouses extend far beyond rent payments to encompass utilities, transportation, food, and miscellaneous expenses that collectively represent substantial monthly financial commitments subject to currency fluctuation impacts. Living costs in Tokyo sharehouses explained reveals how these seemingly minor expenses aggregate into significant monthly obligations that multiply currency risk exposure across multiple spending categories.

Transportation costs, typically ranging from ¥10,000 to ¥20,000 monthly for most sharehouse residents, can swing dramatically based on exchange rate movements, potentially adding or subtracting hundreds of dollars annually from transportation budgets. Food expenses, averaging ¥30,000 to ¥50,000 monthly for most international residents, represent another major category where currency fluctuations directly impact daily purchasing decisions and dietary choices.

Utility bills, internet fees, and shared house expenses create additional layers of currency exposure that compound the overall financial impact of exchange rate movements. Understanding utility bills in Japanese sharehouses becomes more complex when currency fluctuations affect the real cost of heating, electricity, and water consumption throughout different seasons and usage patterns.

The psychological impact of watching daily expenses fluctuate based on global currency markets creates ongoing stress and uncertainty that affects spending behavior, social activities, and overall quality of life for residents who must constantly recalculate the real cost of every purchase and lifestyle choice.

Strategic Budget Planning Under Currency Volatility

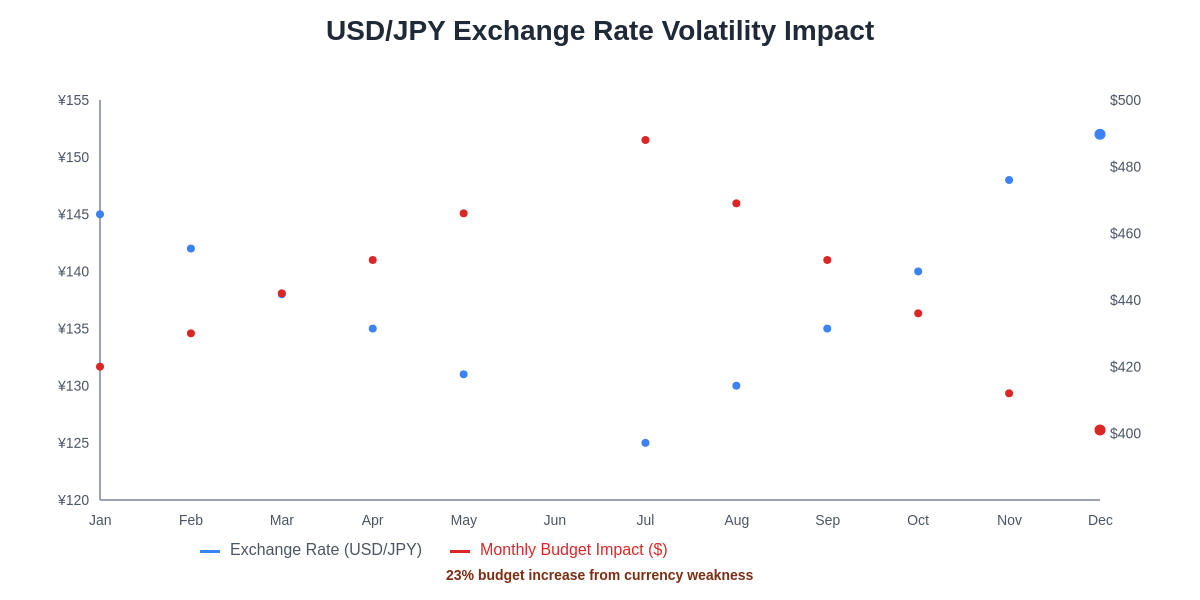

Effective budget planning for international sharehouse residents requires sophisticated strategies that acknowledge currency risk while maintaining practical approaches to daily financial management. How to budget realistically for sharehouse living must account for potential currency swings that can increase total living costs by twenty to forty percent during unfavorable market conditions.

Creating buffer zones within monthly budgets helps absorb currency-driven cost increases without forcing immediate lifestyle changes or emergency borrowing. Financial experts recommend maintaining currency buffers representing fifteen to twenty-five percent of monthly expenses, though this conservative approach may not be practical for students or entry-level workers operating on tight financial margins.

Diversification strategies involving multiple income sources, savings currencies, and expense timing can help reduce overall currency exposure while maintaining financial flexibility during volatile periods. Some residents develop hybrid approaches that combine local yen-denominated income with foreign currency savings to create natural hedging mechanisms that reduce net currency exposure.

Regular monitoring and adjustment of budget assumptions based on currency trends enables proactive financial management that anticipates potential problems before they become critical. How to calculate your true living costs requires ongoing recalibration that reflects current exchange rate realities rather than outdated assumptions based on historical currency levels.

Income and Expense Timing Mismatches

International sharehouse residents frequently face timing mismatches between income receipt and expense obligations that amplify currency risk and create cash flow challenges during volatile market periods. Students receiving quarterly tuition refunds or family support payments may find themselves exposed to several months of currency risk between payment receipts, while professionals receiving monthly salaries in foreign currencies face ongoing exposure to daily exchange rate movements.

The frequency of international money transfers affects both transaction costs and currency exposure, as residents must balance the convenience of frequent transfers against higher cumulative fees and increased exposure to short-term currency volatility. How international money transfers cost more examines how transfer timing and frequency decisions impact overall financial efficiency for international residents.

Seasonal expense patterns common in Japanese living, including higher utility bills during summer air conditioning seasons and winter heating periods, create predictable expense spikes that coincide with unpredictable currency movements. Residents may find themselves facing peak expense periods during unfavorable exchange rate environments, multiplying the financial impact of seasonal cost increases.

Emergency expenses, medical bills, and unexpected sharehouse-related costs cannot be timed to coincide with favorable exchange rates, forcing residents to execute currency conversions during potentially disadvantageous market conditions that amplify the real cost of unexpected financial obligations.

Long-term Financial Planning Challenges

Currency volatility creates profound challenges for long-term financial planning that extend beyond immediate monthly budget management to affect savings goals, investment strategies, and major life decisions for international residents. Why some residents feel constantly judged often relates to financial stress and uncertainty created by currency-driven budget pressures that affect social interactions and community relationships.

Savings accumulation becomes problematic when currency fluctuations can eliminate months of careful budgeting and expense control within days of adverse market movements. Residents may find themselves unable to maintain consistent savings rates or achieve financial milestones due to currency-driven increases in living costs that consume discretionary income traditionally allocated to savings and investments.

Educational financing decisions, including tuition planning and living expense budgeting for multi-year academic programs, require currency risk assessment that extends years into the future. Student sharehouses near top Tokyo universities become more or less affordable over time based on currency trends that can make educational investments financially unsustainable despite careful initial planning.

Career development timelines and professional goal setting must account for currency risk factors that influence the financial viability of extended residence periods, language learning investments, and professional certification pursuits that require consistent financial commitment over extended periods.

Psychological and Social Impacts of Financial Uncertainty

The constant awareness of currency-driven financial vulnerability creates ongoing psychological stress that affects academic performance, social relationships, and overall mental health for international residents living in Tokyo sharehouses. Why some residents become social outcasts often correlates with financial pressures that limit social participation and create isolation during periods of currency-driven budget constraints.

Social activities, dining out, entertainment expenses, and cultural experiences become casualties of currency volatility as residents reduce discretionary spending to maintain essential housing and living expenses during unfavorable exchange rate periods. Making friends through Tokyo sharehouse communities becomes more challenging when financial constraints limit participation in social activities and community building opportunities.

The decision-making paralysis created by currency uncertainty affects housing choices, career opportunities, and personal relationships as residents struggle to make long-term commitments in environments where financial assumptions can change dramatically without warning. Dating while living in Tokyo sharehouses faces additional complications when currency-driven financial stress affects confidence and social participation.

Professional development opportunities, language learning investments, and skill-building activities may be postponed or abandoned when currency fluctuations consume financial resources previously allocated to personal growth and career advancement initiatives.

Risk Mitigation Strategies and Financial Tools

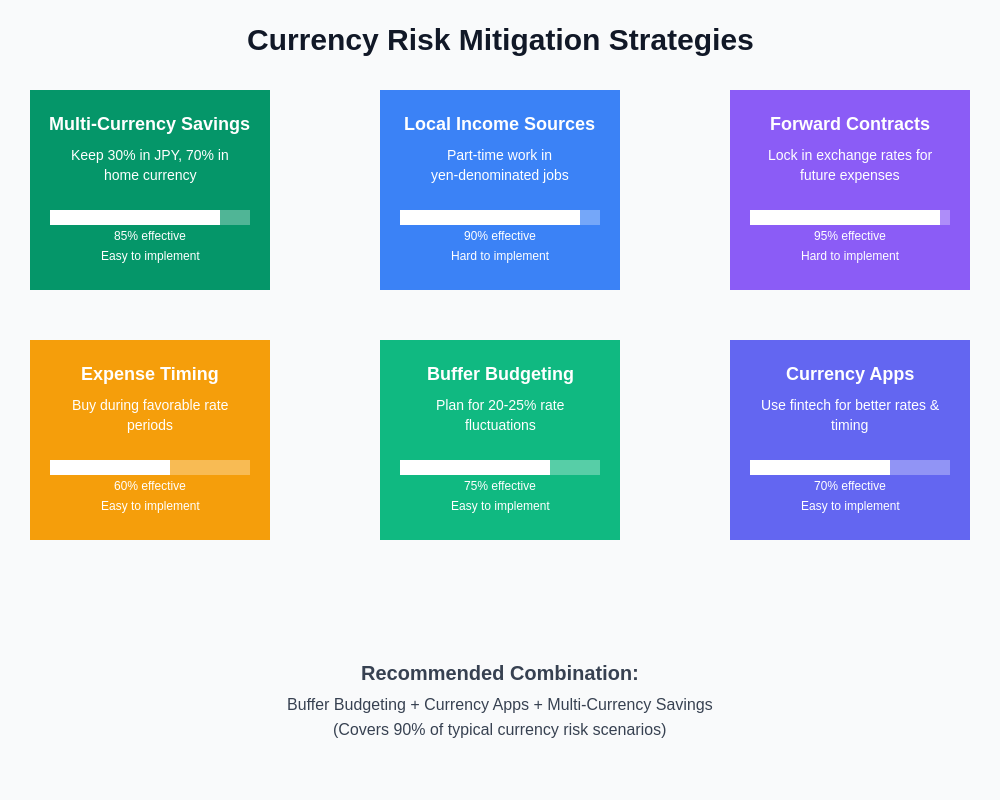

Practical risk mitigation approaches enable international residents to reduce currency exposure while maintaining reasonable access to necessary financial resources for daily living and long-term planning. Forward contracts, currency hedging products, and multi-currency account structures provide sophisticated tools for residents with sufficient financial resources and market knowledge to implement strategic currency management approaches.

Local income development through part-time employment, freelance work, or business activities denominated in yen creates natural currency hedging that reduces net exposure to exchange rate fluctuations. Why some residents become transportation experts often develop local income streams that provide yen cash flow to offset currency risk from foreign-denominated savings and support payments.

Expense timing strategies that accelerate purchases during favorable exchange rate periods and defer discretionary spending during unfavorable periods help optimize purchasing power over time. Bulk purchasing of non-perishable goods, annual transportation passes, and advance payment of sharehouse fees during strong home currency periods can lock in favorable rates for extended periods.

Multi-currency savings strategies that maintain reserves in both yen and home currencies provide flexibility to execute currency conversions during favorable market conditions while maintaining emergency funds accessible regardless of short-term exchange rate movements.

These proven strategies offer different levels of effectiveness and implementation difficulty, allowing residents to choose approaches that match their financial resources and risk tolerance levels.

Technology Solutions and Monitoring Tools

Modern financial technology provides international residents with sophisticated tools for monitoring currency movements, executing cost-effective international transfers, and managing multi-currency financial obligations with greater efficiency and lower costs than traditional banking approaches. Currency monitoring applications, rate alert systems, and automated transfer scheduling help residents optimize timing and minimize transaction costs for necessary currency conversions.

Digital banking platforms specializing in international transfers often provide better exchange rates and lower fees than traditional banks, enabling residents to reduce the cost impact of necessary currency conversions while maintaining access to needed yen funding for monthly expenses. Why some residents become more open-minded often discover innovative financial tools and strategies through sharehouse community knowledge sharing.

Budgeting applications with multi-currency support enable real-time tracking of exchange rate impacts on monthly expenses, providing immediate visibility into currency-driven budget changes that affect spending decisions and financial planning. Expense categorization and trend analysis tools help identify which spending categories face the greatest currency risk exposure.

Automated savings and investment platforms that support multi-currency operations enable residents to maintain diversified financial positions that reduce overall currency risk while pursuing long-term financial goals despite short-term exchange rate volatility.

Building Resilient Financial Frameworks

Successful management of currency risk requires building financial frameworks that acknowledge volatility while maintaining practical approaches to daily expense management and long-term financial planning. Emergency fund sizing must reflect potential currency-driven cost increases, requiring larger reserves than domestic residents typically maintain to handle the same level of unexpected expenses.

Income diversification strategies that combine local and foreign currency sources create stability that reduces net currency exposure while providing flexibility during volatile market periods. Why some residents develop better communication skills often learn to negotiate payment terms, explore local earning opportunities, and build financial networks that provide stability during challenging currency environments.

Regular financial plan reviews and assumption updates ensure that budget frameworks reflect current market realities rather than outdated exchange rate assumptions that no longer provide accurate guidance for spending and savings decisions. Flexibility and adaptability in financial planning become essential skills for managing long-term residence in volatile currency environments.

Community knowledge sharing through sharehouse networks enables residents to learn from others’ experiences with currency management, discover new tools and strategies, and build support systems that provide guidance during challenging financial periods created by adverse currency movements.

The mastery of currency risk management represents a crucial life skill for international residents that extends far beyond sharehouse living to affect career development, investment strategies, and global mobility throughout their professional and personal lives. Understanding these dynamics empowers residents to make informed decisions that protect their financial stability while pursuing their educational, professional, and personal goals in one of the world’s most dynamic international cities.

Disclaimer

This article is for informational purposes only and does not constitute professional financial advice. Exchange rates and currency markets are subject to extreme volatility influenced by factors beyond individual control. Readers should consult with qualified financial advisors and conduct their own research before implementing currency risk management strategies. Past exchange rate performance does not predict future currency movements, and all international residents should prepare for potential adverse currency scenarios that could significantly impact their financial situations.