The freelance lifestyle that offers freedom and flexibility in many countries transforms into a significant liability when navigating Tokyo’s conservative sharehouse rental market, where property managers and landlords view irregular income patterns as fundamental risks that disqualify applicants regardless of their actual financial stability or professional success. This systematic discrimination against freelance professionals creates barriers that extend far beyond simple income verification, encompassing cultural biases about employment stability, bureaucratic requirements designed for traditional employment structures, and risk assessment frameworks that fail to account for modern work realities.

The psychological toll of constant application rejections affects freelancers’ confidence and mental health while forcing them into increasingly desperate housing situations that compromise their professional goals and financial stability in ways that traditional employees rarely experience. Understanding why freelance income creates such profound application difficulties requires examining the intersection of Japanese employment culture, rental industry practices, and bureaucratic systems that systematically disadvantage non-traditional workers seeking accommodation in Tokyo’s competitive housing market.

Traditional Employment Bias in Japanese Rental Culture

Japanese rental culture’s deep-rooted preference for traditional employment structures reflects broader cultural values that prioritize stability, predictability, and institutional affiliation over individual achievement or financial capability, creating systematic discrimination against freelancers whose professional success cannot be easily categorized within conventional employment frameworks. How employment status impacts sharehouse approval demonstrates the extent of this bias, but the cultural foundations run deeper than simple risk assessment into fundamental assumptions about social status and reliability.

Property managers and landlords often view freelance work as inherently unstable regardless of income levels or professional track records, reflecting cultural biases that associate employment security with corporate affiliation rather than individual financial performance or professional expertise. This perception creates immediate disqualification scenarios where freelancers with substantial savings and consistent income streams face rejection while traditionally employed individuals with lower incomes and minimal savings receive approval based solely on their employment classification.

The Japanese concept of “shakaijin” (functioning member of society) traditionally requires corporate employment verification that freelancers cannot provide, creating cultural barriers that extend beyond financial qualification into social acceptability within rental community contexts. Property managers often worry that freelancers will not integrate properly into sharehouse communities or maintain the social harmony expected in shared living environments, reflecting broader cultural assumptions about professional identity and social responsibility.

Risk assessment frameworks used by rental companies assume that corporate employment provides guarantee mechanisms through HR departments, payroll consistency, and institutional backing that freelancers cannot replicate through individual financial documentation, regardless of their actual earning capacity or financial management skills. The institutional preference for risk transfer to corporate entities rather than individual assessment creates systematic exclusion patterns that affect even highly successful freelance professionals.

Documentation Challenges and Verification Complexities

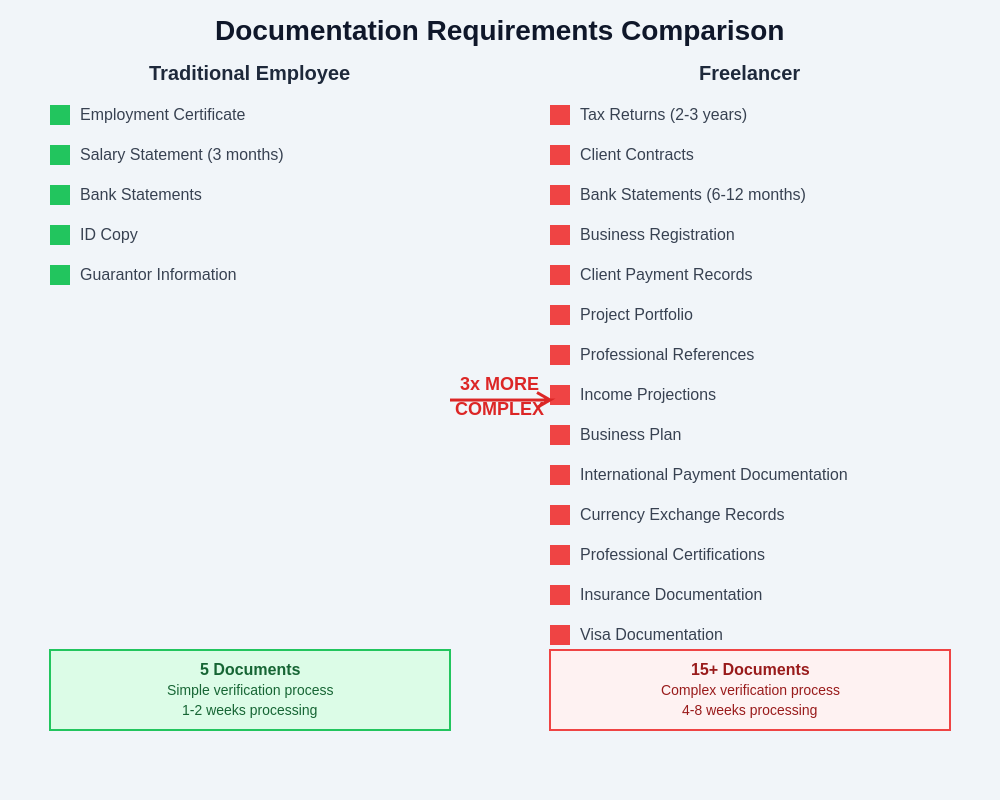

Income verification requirements designed for traditional employment structures create impossible documentation challenges for freelancers whose financial records do not conform to standardized payroll formats that rental applications expect, forcing them to translate complex business financial data into simplified employment verification categories that misrepresent their actual financial situations. What documents you need for Tokyo sharehouse applications outlines standard requirements, but freelancers face additional documentation burdens that traditional employees never encounter.

Tax documentation for freelance income often requires complex explanations and translations that property managers cannot easily interpret or verify, particularly when dealing with international clients, multiple income streams, or business expense deductions that affect reported income figures but do not reflect actual earning capacity or financial stability. The complexity of freelance tax structures often creates confusion during application reviews where simple salary verification would provide clear qualification metrics.

Bank statement patterns for freelancers show irregular deposit schedules that trigger automatic red flags in rental application systems designed to identify consistent monthly income patterns, even when total annual earnings significantly exceed requirements and financial reserves demonstrate strong fiscal management. The temporal mismatch between freelance payment cycles and monthly rent obligations creates perceived risk factors that override actual financial capability assessments.

Client payment documentation requires extensive explanation and verification processes that extend application timelines while creating additional administrative burdens for property managers who prefer streamlined approval processes with minimal verification requirements. The international nature of many freelance businesses creates additional complexity through currency conversions, international payment systems, and client verification challenges that domestic employment verification never encounters.

Contract and project documentation must demonstrate income continuity and future earning potential through client agreements and project pipelines that property managers cannot easily evaluate or verify, requiring specialized knowledge about freelance business operations that rental industry professionals typically lack. The project-based nature of freelance work creates challenges in proving long-term income stability that traditional employment contracts provide automatically.

The documentation burden for freelancers exceeds traditional employment requirements by a factor of three, creating additional barriers that many property managers view as red flags rather than thorough preparation.

Irregular Income Patterns and Payment Cycles

Monthly rent obligations conflict fundamentally with freelance payment cycles that often involve quarterly payments, project-based compensation, or seasonal earning patterns that create cash flow challenges during application periods when consistent monthly income verification becomes essential for approval consideration. How to budget realistically for sharehouse living addresses budgeting challenges, but irregular income patterns create unique obstacles that standard budgeting advice cannot resolve.

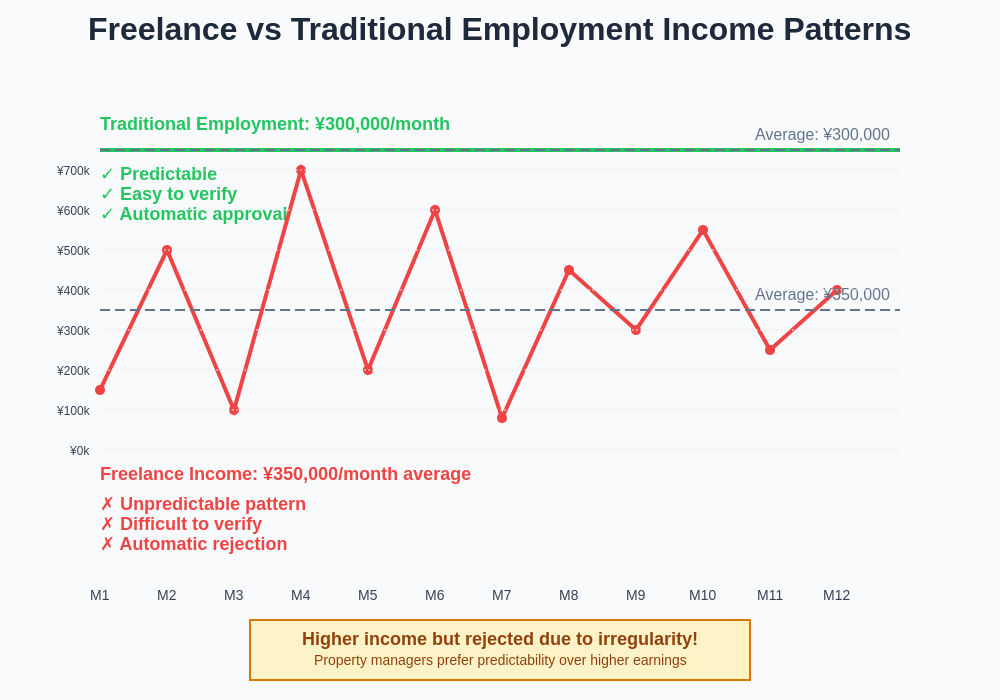

Seasonal fluctuations in freelance earnings create periods of high income followed by lean months that average out to stable annual earnings but appear as income instability when viewed through monthly assessment frameworks that rental applications typically employ. Property managers focus on worst-month scenarios rather than annual earning averages, creating qualification challenges during natural business cycle low points that traditional employees never experience.

Project payment delays beyond freelancers’ control can create temporary cash flow gaps that coincide with application periods, forcing freelancers to apply during financial low points that misrepresent their typical earning capacity and financial stability. The inability to control payment timing creates application timing challenges that can result in rejections based on temporary financial situations rather than overall earning patterns.

Client payment disputes or delayed invoicing can create months-long gaps in documented income that appear as employment instability during application review periods, even when freelancers maintain active client relationships and ongoing project work that will generate future payments. The lag between work completion and payment receipt creates documentation gaps that rental applications cannot accommodate through standard verification processes.

Currency exchange fluctuations for international freelance work create additional income variability that appears as instability when converted to yen for rental applications, even when the underlying work volume and client payments remain consistent in the original currencies. International freelancers face double volatility through both payment timing irregularities and currency conversion unpredictability that compounds income verification challenges.

The stark contrast between predictable traditional employment income and irregular freelance patterns reveals why property managers consistently favor traditional employees despite freelancers often earning higher annual totals.

Guarantor Requirements and Professional Networking Challenges

Japanese rental applications typically require guarantors with traditional employment who can verify their own income stability and agree to financial liability for tenant obligations, creating additional barriers for freelancers who often lack professional networks with traditionally employed contacts willing to accept guarantor responsibilities. Why some sharehouses require Japanese guarantors explains guarantor requirements, but freelancers face unique challenges in meeting these social and professional networking demands.

Professional networks for freelancers often consist of other freelancers, international clients, or industry contacts who cannot serve as guarantors due to their own non-traditional employment status or geographic location, creating systemic exclusion from guarantor-based approval processes that assume traditional employment social networks. The freelance community’s lack of traditional corporate relationships creates mutual support gaps in rental application contexts.

Language barriers affect freelance guarantor arrangements more severely because potential guarantors must understand complex business income explanations and take responsibility for financial obligations related to irregular income patterns that they may not fully comprehend or feel comfortable guaranteeing. The additional complexity of explaining freelance income structures to potential guarantors creates communication challenges that traditional employment verification avoids.

Cultural expectations around guarantor relationships assume workplace or family connections that provide ongoing contact and monitoring capabilities, but freelance professional relationships often lack the sustained personal contact that Japanese guarantor customs expect for effective risk management and communication during potential problems. The project-based nature of freelance relationships creates temporary rather than sustained professional connections that guarantor requirements assume.

Professional guarantor services that cater to international residents often charge premium fees for freelance applicants due to perceived income instability, creating additional financial barriers that traditional employees do not face while applying for similar housing options. The risk premium for freelance guarantor services compounds the existing financial challenges that irregular income patterns create for housing searches.

Visa Status Complications and Legal Framework Issues

Freelance work visa categories in Japan often carry additional restrictions and renewal uncertainties that property managers view as long-term risks affecting lease stability and payment continuity, creating systematic discrimination against visa types associated with freelance work regardless of individual financial qualifications or professional success. How visa status affects your sharehouse application outlines visa considerations, but freelancers face compounded challenges through both income irregularity and visa category concerns.

Visa renewal requirements for freelance professionals often depend on income thresholds and client documentation that create annual uncertainty about continued legal residence status, making property managers reluctant to approve lease agreements with freelancers whose legal status may change during the rental period. The annual visa renewal process creates ongoing instability perceptions that affect multi-year lease qualification even for established freelance professionals.

Tax obligation complications for freelance professionals include complex reporting requirements and potential liability issues that property managers may not understand but perceive as legal risks that could affect tenant reliability or create administrative complications during the rental relationship. The complexity of freelance tax status creates additional perceived risks beyond simple income verification concerns.

Business registration requirements for certain types of freelance work in Japan create additional documentation and legal compliance obligations that property managers may view as complicating factors rather than legitimizing business activities, particularly when freelancers operate through international platforms or clients that Japanese rental industry professionals cannot easily verify or understand.

Immigration law changes that affect freelance visa categories create ongoing uncertainty about legal status stability that property managers factor into long-term rental risk assessments, making them reluctant to approve applications from freelancers whose visa categories may face future regulatory changes that could affect their continued residence eligibility.

Bank Account and Financial System Challenges

Japanese banking systems often discriminate against freelance account holders through higher fee structures, reduced credit access, and additional documentation requirements that create financial system barriers extending beyond rental applications into broader financial exclusion that affects housing qualification indirectly through reduced financial services access. The systematic financial discrimination against freelancers creates cascading effects that impact housing applications through multiple pathways.

Credit history development proves more difficult for freelancers who may not qualify for traditional credit products due to irregular income patterns, creating circular exclusion where lack of credit history affects rental applications while irregular income prevents credit establishment that would improve rental qualification. The credit system’s bias toward traditional employment creates long-term financial barriers that compound housing access challenges.

International banking complications for freelancers working with overseas clients create additional documentation complexity and verification challenges when rental applications require domestic banking verification and income source documentation. The international nature of freelance businesses often conflicts with domestic financial verification requirements that rental applications assume.

Business expense deductions that reduce reported taxable income for freelancers can create misleading income documentation that understates actual earning capacity while providing tax advantages, forcing freelancers to choose between tax optimization and rental application qualification when reported income figures become primary approval criteria. The tension between tax efficiency and rental qualification creates financial strategy conflicts unique to freelance professionals.

Banking relationship development requires time and consistent deposit patterns that new freelancers may not have established, creating additional barriers for freelancers who are establishing businesses in Japan while simultaneously seeking housing approval based on banking relationships that require time to develop adequately for rental qualification purposes.

Alternative Income Verification Strategies

Portfolio diversification through multiple client relationships and income streams can actually strengthen financial stability compared to single-employer dependence, but rental applications lack frameworks for evaluating diversified income sources that may provide superior risk distribution compared to traditional employment vulnerability to single company failures or industry downturns. Freelancers must develop presentation strategies that highlight income diversification advantages rather than allowing property managers to view multiple income sources as instability indicators.

Professional references from long-term clients can provide alternative verification of income stability and professional reliability that substitutes for traditional employment verification, but requires careful cultivation of client relationships and willingness from clients to participate in rental verification processes that they may not understand or feel comfortable supporting. Building client relationships that extend beyond project work into personal professional references requires additional effort that traditional employees do not need to invest.

Financial planning documentation that demonstrates savings patterns, emergency fund development, and financial management skills can provide evidence of financial responsibility that may overcome concerns about irregular income patterns, but requires sophisticated financial record-keeping and presentation skills that traditional salary verification does not demand. Freelancers must become financial planners and presenters in ways that traditional employees never encounter during rental applications.

Professional portfolio documentation including client testimonials, project histories, and industry recognition can demonstrate professional stability and future earning potential that income documentation alone cannot convey, but requires comprehensive professional documentation that most traditional employment verification processes do not require or evaluate. The additional documentation burden for freelancers creates application complexity that extends far beyond simple financial verification.

Industry expertise demonstration through certifications, professional memberships, and specialized skills documentation can provide context for income patterns and future earning potential that generic income verification cannot capture, but requires ongoing professional development investment and documentation that traditional employment verification assumes through job titles and company affiliations.

Financial Planning and Application Timing Strategies

Strategic application timing around high-income periods can maximize qualification chances by aligning applications with peak earning documentation, but requires careful financial planning and income forecasting that traditional employees never need to consider when timing rental applications. Freelancers must become strategic planners around their business cycles in ways that extend beyond simple housing searches into comprehensive business and housing coordination.

Cash flow management becomes critical for freelancers who must maintain sufficient liquid reserves for rental deposits and first-month payments while managing irregular income patterns that may not align with housing availability and application timing requirements. The financial planning complexity for freelancers extends beyond normal budgeting into cash flow optimization that traditional salary earners rarely encounter.

Emergency fund requirements for freelancers must account for both business income fluctuations and potential rental deposit forfeitures when applications fail due to income verification issues, creating dual financial risk management challenges that traditional employees do not face when planning housing transitions. The financial buffer requirements for freelancers exceed standard emergency fund recommendations due to compounded risks from both business operations and housing qualification challenges.

Business development timing must consider housing stability needs when planning client acquisition, project timing, and income optimization strategies that affect rental qualification while simultaneously supporting business growth objectives. Freelancers must coordinate business development with housing needs in ways that create complex planning requirements beyond either business or housing considerations alone.

Professional service investment in financial advisors, tax professionals, and legal consultants may become necessary for freelancers to optimize their application materials and income presentation, creating additional business expenses that traditional employees do not incur when seeking housing. The professional service requirements for successful rental applications add business costs that must be factored into freelance pricing and financial planning strategies.

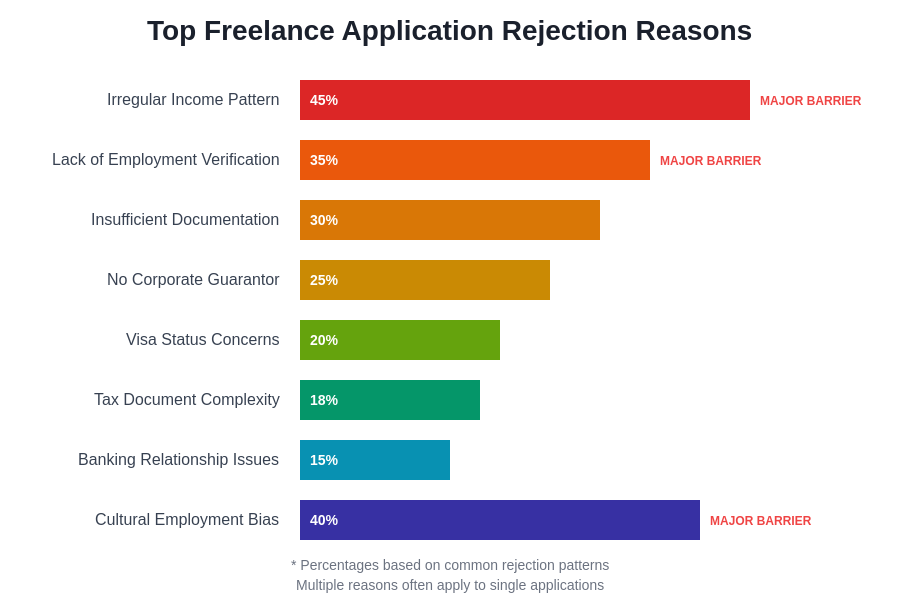

Multiple rejection factors typically combine to create systematic exclusion of freelance applicants, with irregular income patterns and cultural employment bias representing the most significant barriers to approval.

Understanding and overcoming the systematic barriers that freelance income creates in Tokyo’s sharehouse rental market requires comprehensive preparation, strategic planning, and professional presentation skills that extend far beyond traditional housing searches into sophisticated business and financial management practices. Freelancers who recognize these challenges and develop appropriate strategies find themselves better prepared to navigate the complex intersection of non-traditional employment and conservative rental markets while maintaining the professional flexibility that drew them to freelance careers in the first place.

Disclaimer

This article is for informational purposes only and does not constitute professional legal, financial, or immigration advice. Rental requirements and application processes vary significantly between properties and management companies. Freelancers should consult with qualified professionals regarding their specific situations and develop appropriate documentation and application strategies. Success in rental applications depends on multiple factors beyond income verification, and individual experiences may vary significantly based on specific circumstances and market conditions.