International money transfers represent one of the most significant yet poorly understood financial burdens facing foreign residents living in sharehouses across Tokyo and Japan. The complexity of global banking systems, regulatory frameworks, and currency exchange mechanisms creates a labyrinthine structure of fees and charges that can consume substantial portions of transferred funds, particularly impacting those managing monthly rent payments, family support obligations, and personal savings movements between countries.

Understanding the intricate web of costs associated with international money transfers becomes crucial for residents managing tight budgets while living in Tokyo sharehouses, where every yen matters for maintaining financial stability. How international money transfers affect monthly payments demonstrates the real-world impact these costs have on daily living expenses and long-term financial planning for international residents.

The Complex Architecture of International Banking

The global financial system operates through an intricate network of correspondent banking relationships, intermediary institutions, and regulatory compliance mechanisms that create multiple layers of cost accumulation throughout the international transfer process. Traditional banking institutions maintain relationships with hundreds of foreign banks worldwide, each requiring separate agreements, compliance protocols, and technological integration that generates operational overhead reflected in transfer fees.

When funds travel from one country to another, they rarely follow direct paths between origin and destination banks, instead moving through multiple intermediary institutions that each extract processing fees and margin adjustments. How banking fees add up for foreign residents illustrates how these incremental charges compound into substantial total costs that significantly impact monthly budgets for sharehouse residents.

The correspondent banking system requires significant infrastructure investments, staff training, and technology maintenance that banks recover through various fee structures imposed on international transfer services. Smaller regional banks often lack direct relationships with foreign institutions, necessitating multiple intermediary steps that multiply costs and extend processing timeframes beyond domestic transfer expectations.

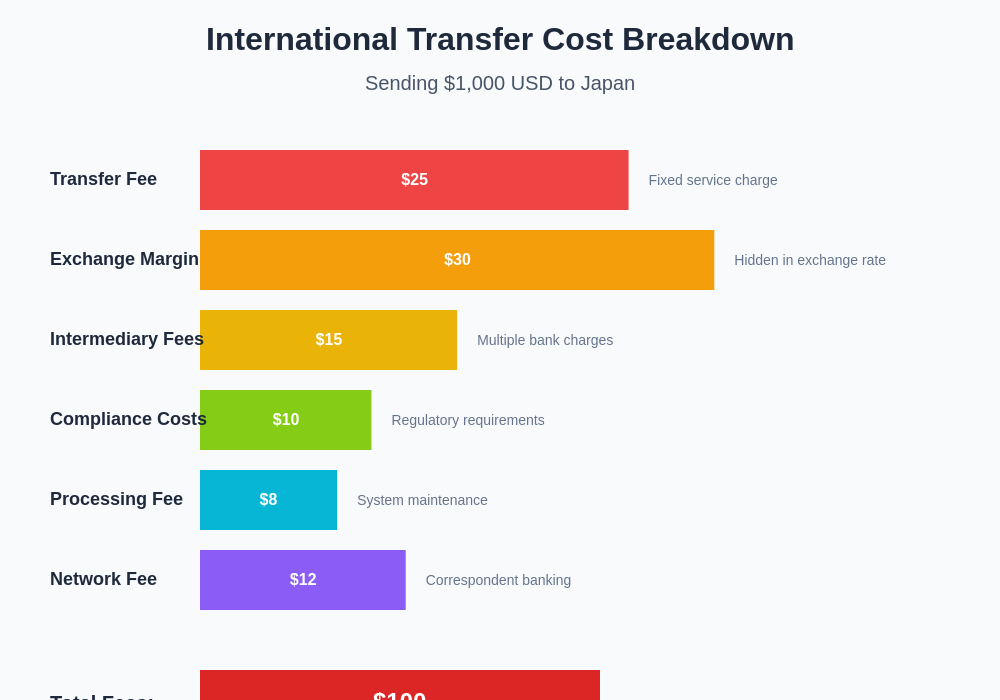

This visualization demonstrates how fees accumulate at each step of the international transfer process, with multiple intermediaries each extracting charges that compound into substantial total costs for the sender.

Currency Exchange Rate Manipulation and Hidden Margins

Currency exchange represents perhaps the most opaque and profitable aspect of international money transfers, where financial institutions embed substantial margins within seemingly competitive exchange rates that customers rarely recognize or understand. Banks typically offer exchange rates that differ significantly from interbank market rates, capturing spreads that can range from two to four percent of total transfer amounts without explicitly advertising these charges as fees.

The practice of embedding currency margins within exchange rates creates an invisible tax on international transfers that becomes particularly burdensome for residents making regular monthly payments or supporting family members abroad. How currency exchange affects monthly payments explores the cumulative impact of these hidden charges on long-term financial planning and budget management.

Real-time currency fluctuations provide additional opportunities for financial institutions to capture profits through timing differences between rate quotations and actual transaction execution, particularly during volatile market periods when exchange rates change rapidly throughout trading days. These temporal margins often escape customer attention while contributing significantly to overall transfer costs.

Financial institutions maintain different exchange rate tiers based on transfer amounts, customer relationships, and service types, creating complex pricing structures that make direct cost comparisons extremely difficult for average consumers seeking optimal transfer solutions.

Breaking down the various cost components reveals how seemingly small fees and margins accumulate into significant total expenses that can consume ten percent or more of transferred amounts.

Regulatory Compliance and Anti-Money Laundering Costs

International regulatory requirements impose substantial compliance burdens on financial institutions processing cross-border transfers, with costs ultimately passed to consumers through various fee structures and service charges. Anti-money laundering protocols require extensive documentation, identity verification, and transaction monitoring systems that demand significant technological and human resource investments from banking institutions.

Know Your Customer regulations mandate detailed record-keeping, background checks, and ongoing surveillance of international transfer patterns that create operational overhead reflected in transfer pricing structures. How legal disputes get resolved in sharehouses touches on the broader regulatory environment affecting international residents’ financial transactions and legal obligations.

Sanctions screening systems must evaluate every international transfer against constantly updated lists of prohibited individuals, organizations, and countries, requiring sophisticated technology platforms and specialized personnel that contribute to overall service costs. These compliance mechanisms often cause transfer delays and additional documentation requirements that further increase operational expenses.

Different countries maintain varying regulatory standards and reporting requirements that necessitate customized compliance approaches for each destination market, multiplying the complexity and cost of maintaining international transfer services across global banking networks.

Technology Infrastructure and Security Investment Requirements

Modern international money transfer systems require substantial investments in cybersecurity, fraud prevention, and technological infrastructure that financial institutions recover through transfer fees and service charges. The constant threat of financial cybercrime necessitates ongoing security upgrades, monitoring systems, and incident response capabilities that generate significant operational costs.

Real-time transfer capabilities demand sophisticated technological platforms capable of communicating with banking systems worldwide while maintaining security protocols and regulatory compliance throughout transaction processing. How smart locks change sharehouse security demonstrates how technology investments in security features ultimately affect cost structures across various service industries.

Legacy banking systems often require expensive integration work to communicate with modern transfer platforms, creating technical debt and maintenance costs that contribute to overall service pricing. The need to maintain compatibility with hundreds of different banking systems worldwide multiplies technological complexity and associated infrastructure costs.

Data storage and processing requirements for international transfers generate ongoing operational expenses through server maintenance, backup systems, and disaster recovery capabilities that ensure service continuity and regulatory compliance across different jurisdictions.

Market Competition Limitations and Oligopolistic Pricing

The international money transfer market operates under significant barriers to entry that limit competitive pressure and enable established institutions to maintain higher pricing structures than would exist in truly competitive markets. Regulatory licensing requirements, capital reserves, and compliance infrastructure create substantial startup costs that discourage new market entrants and protect existing service providers.

Major financial institutions often coordinate pricing strategies through industry associations and regulatory bodies, creating informal pricing floors that prevent aggressive competition on transfer fees and exchange rate margins. How group buying power reduces individual costs illustrates how market concentration affects pricing power and consumer options across various service categories.

Network effects create additional competitive advantages for established transfer providers, as banks with extensive correspondent relationships can offer broader destination coverage and faster processing times that justify premium pricing to customers requiring reliable international transfer services.

Customer switching costs remain high due to account setup requirements, relationship building, and learning curves associated with different transfer platforms, enabling existing providers to maintain pricing power even when more competitive alternatives become available in the marketplace.

Geographic and Infrastructure Disadvantages

Certain regions and countries face higher international transfer costs due to limited banking infrastructure, political instability, or regulatory restrictions that increase operational risks and compliance requirements for financial institutions. Remote or economically unstable destinations often require additional intermediary banks and specialized handling procedures that multiply transfer costs beyond standard international rates.

How distance from city center changes living experience parallels how geographic factors affect service costs and availability across different markets and regions. Countries with weak banking systems or limited technological infrastructure require additional verification steps and manual processing that increase both costs and processing timeframes.

Currency stability and convertibility issues in certain markets create additional risks for financial institutions that must be compensated through higher fees and less favorable exchange rates offered to customers sending funds to these destinations.

Time zone differences and business hour misalignments between origin and destination countries can extend processing times and require specialized staffing arrangements that contribute to overall service costs for international transfers.

Alternative Transfer Methods and Emerging Competition

Digital payment platforms and fintech companies have emerged as competitive alternatives to traditional banking channels, often offering more transparent pricing and lower overall costs for international money transfers. How digital entertainment replaces social interaction reflects broader technological disruption patterns affecting traditional service industries and consumer behavior.

Cryptocurrency and blockchain-based transfer systems promise to eliminate many intermediary costs associated with traditional banking networks, though regulatory uncertainty and technical complexity limit mainstream adoption for routine international transfers. These emerging technologies face significant scaling challenges and regulatory obstacles that prevent them from fully replacing established transfer mechanisms.

Peer-to-peer transfer networks attempt to bypass traditional banking systems by matching individuals seeking to exchange currencies in different countries, potentially offering better rates but introducing additional risks and complexity that many users find prohibitive for regular use.

Central bank digital currencies and government-backed transfer systems represent potential future alternatives that could significantly reduce international transfer costs by eliminating private sector profit margins and intermediary fees, though implementation timelines remain uncertain across most major economies.

Modern fintech solutions often provide substantially lower costs and better service compared to traditional banking channels, though availability and reliability can vary by destination country and transfer amount.

Impact on Sharehouse Residents and Budget Planning

International transfer costs create particular challenges for sharehouse residents who must manage monthly rent payments, utility contributions, and personal expenses while maintaining financial connections to home countries for family support or savings management. How to budget realistically for sharehouse living provides frameworks for incorporating transfer costs into monthly financial planning.

Regular transfer requirements for rent payments or family support create cumulative cost burdens that can consume significant percentages of monthly income, particularly affecting students and entry-level workers living in budget-conscious sharehouse arrangements. These recurring fees often exceed initial estimates and require ongoing budget adjustments to maintain financial stability.

Emergency transfer needs during medical situations, family crises, or unexpected expenses often involve expedited processing fees that can double or triple normal transfer costs, creating additional financial stress during already challenging circumstances. How emergency expenses are never budgeted explores the broader challenge of planning for unexpected financial requirements while living abroad.

Currency fluctuations can create additional uncertainty in transfer costs and recipient amounts, making precise budget planning difficult for residents dependent on international transfers for essential living expenses and sharehouse payments.

Strategies for Minimizing Transfer Costs

Understanding fee structures and comparing total costs across multiple service providers enables more informed decision-making about international transfer methods and timing strategies that can reduce overall expenses. How to calculate your true living costs provides methodologies for evaluating all-inclusive costs including hidden fees and charges.

Consolidating multiple smaller transfers into less frequent larger amounts can reduce per-transaction fees and improve exchange rate margins, though this strategy requires careful cash flow management and may not suit all residents’ financial circumstances or payment obligations.

Timing transfers during favorable exchange rate periods and avoiding peak demand times can sometimes yield better rates and lower fees, though this requires market monitoring and flexibility in transfer scheduling that may not align with mandatory payment deadlines.

Building relationships with specific financial institutions and maintaining higher account balances can sometimes qualify residents for preferential transfer rates and reduced fees, though these strategies require significant capital commitments that may exceed many residents’ financial capabilities.

The complex landscape of international money transfer costs reflects fundamental structural characteristics of global banking systems, regulatory requirements, and market dynamics that create inherent expense burdens for cross-border financial transactions. Understanding these underlying factors empowers sharehouse residents and international workers to make more informed decisions about transfer methods, timing strategies, and budget planning approaches that minimize unnecessary costs while maintaining essential financial connections across borders.

For international residents navigating the challenges of sharehouse living in Tokyo, developing comprehensive awareness of transfer cost structures and available alternatives represents a crucial component of successful long-term financial management and budgetary control in an already expensive metropolitan environment.

Disclaimer

This article is for informational purposes only and does not constitute financial advice. Exchange rates, fees, and transfer costs vary significantly between providers and change frequently based on market conditions and regulatory requirements. Readers should research current options and consult with financial professionals when making decisions about international money transfers. The effectiveness of cost-reduction strategies may vary depending on individual circumstances, transfer amounts, and destination countries.