Living in shared spaces fundamentally alters your legal and financial exposure in ways that many residents fail to recognize until problems arise. The interconnected nature of sharehouse living creates complex liability scenarios where individual actions can trigger cascading consequences affecting multiple parties, property owners, and insurance providers. Understanding these heightened risks becomes essential for protecting yourself financially and legally while navigating the unique challenges that emerge when private living intersects with communal responsibility.

The traditional apartment rental model provides clear boundaries between individual responsibility and external liability, but sharehouses blur these distinctions through shared facilities, communal activities, and overlapping insurance coverage that can leave residents vulnerable to unexpected claims and financial obligations. This complexity multiplies when cultural differences, language barriers, and varying legal understanding among international residents create additional layers of potential misunderstanding and exposure.

The Foundation of Shared Liability Risk

Shared living environments inherently increase personal liability exposure through the multiplication of potential risk factors and the reduction of individual control over environmental hazards. Unlike private apartments where you bear responsibility primarily for your own actions and negligence, sharehouses create scenarios where other residents’ behaviors, maintenance decisions, and emergency responses can directly impact your legal and financial standing.

The physical infrastructure of sharehouses presents particular challenges, as aging buildings converted for multiple occupancy often lack the safety features and maintenance standards found in purpose-built residential complexes. Understanding why some buildings lack proper ventilation illustrates how structural deficiencies can create liability exposure that extends beyond individual tenant responsibility to encompass building-wide safety concerns.

Property management practices in sharehouses frequently operate under different standards than traditional rental arrangements, with cost-cutting measures and high tenant turnover contributing to delayed maintenance, inadequate safety inspections, and unclear responsibility chains when accidents or damage occur. These operational deficiencies create environments where liability questions become complex and potentially expensive to resolve.

The communal nature of sharehouse facilities means that kitchen fires, bathroom floods, or electrical failures can affect multiple residents simultaneously while creating ambiguous responsibility scenarios that complicate insurance claims and legal determinations. Understanding why kitchen fire safety becomes critical demonstrates how shared facility risks can escalate quickly and impact entire buildings.

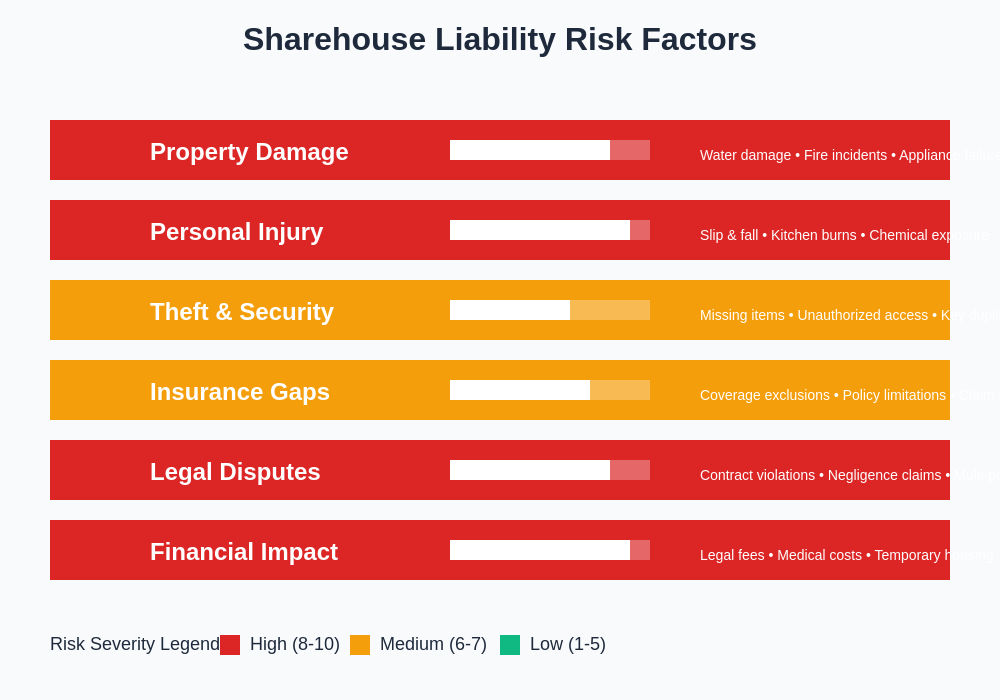

The risk assessment matrix above illustrates how various liability factors in sharehouses create different levels of exposure, with personal injury and financial impact representing the highest severity threats that residents must actively manage and protect against.

Property Damage and Shared Responsibility Complexities

Property damage in sharehouses creates particularly complex liability scenarios because determining individual responsibility becomes challenging when multiple residents have access to shared facilities and common areas. Traditional damage assessment assumes clear ownership and usage patterns, but shared environments make causation difficult to establish and responsibility harder to assign fairly.

Water damage represents one of the most common and expensive liability issues in sharehouses, as plumbing failures, overflowing bathtubs, or washing machine malfunctions can affect multiple units and residents while creating disputes over who bears financial responsibility. Understanding why water quality varies by building age highlights infrastructure issues that can contribute to water-related damage and liability concerns.

Kitchen-related incidents pose significant liability risks due to the concentration of potential hazards including cooking fires, grease accumulation, appliance malfunctions, and food-related accidents that can trigger expensive cleanup requirements and temporary displacement costs for affected residents. Understanding why kitchen politics actually work in Japanese sharehouses reveals the social dynamics that can complicate damage responsibility and resolution processes.

The shared ownership model of common area furnishings and appliances creates additional liability exposure when items break, cause injuries, or require expensive repairs or replacements. Determining financial responsibility among residents who have varying usage patterns, care standards, and financial capabilities often leads to disputes and unexpected costs.

Personal Injury and Negligence Claims

Personal injury risks increase substantially in shared environments due to the combination of higher foot traffic, varied maintenance standards, and the potential for resident negligence to affect other occupants. Slip and fall accidents, burns from shared appliances, or injuries from poorly maintained facilities can result in significant medical costs and legal claims that extend beyond the injured party to encompass other residents and property managers.

The presence of multiple residents with different cultural backgrounds and safety awareness levels creates scenarios where one person’s negligent behavior can expose others to injury liability. Understanding why cultural differences affect friendship building illustrates how varied expectations and communication styles can contribute to safety misunderstandings and liability exposure.

Bathroom and kitchen facilities present particular injury risks due to wet surfaces, sharp objects, hot appliances, and cleaning chemicals that can cause serious injuries when proper safety protocols are not maintained or clearly communicated among residents. The shared nature of these facilities means that injury prevention requires coordination and cooperation that may not exist in houses with poor communication or cultural barriers.

Guest policies in sharehouses can significantly increase personal injury liability exposure, as residents may be held responsible for injuries sustained by their visitors in common areas or through shared facility usage. Understanding why guest policies affect your social life explores how visitor arrangements can create unexpected liability scenarios for residents.

Insurance Coverage Gaps and Complications

Standard renters insurance policies often contain exclusions or limitations that reduce coverage effectiveness in shared living situations, leaving residents with significant gaps in liability protection precisely when their exposure levels are highest. The communal nature of sharehouses can trigger policy exclusions related to business use, multiple occupancy, or shared liability that leave residents financially vulnerable.

Personal property insurance becomes complicated in sharehouses where determining ownership of damaged or stolen items may be difficult, particularly for shared purchases, common area items, or belongings that have been borrowed or moved between residents. Understanding why personal belongings disappear despite locks highlights security issues that can complicate insurance claims and create liability disputes among residents.

Liability coverage limits that seem adequate for individual apartment living may prove insufficient when sharehouse incidents affect multiple parties, involve expensive property damage, or trigger legal claims from injured third parties. The interconnected nature of shared living can amplify financial exposure beyond what standard insurance policies anticipate or cover.

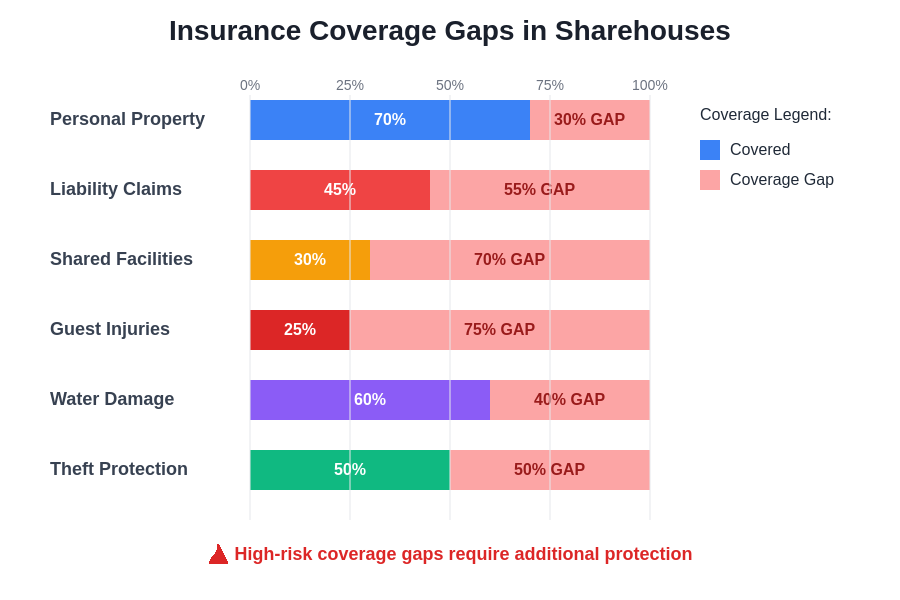

This coverage analysis reveals significant gaps in standard insurance policies when applied to sharehouse living situations, with guest injuries and shared facility coverage showing the most concerning protection deficiencies that residents should address through supplemental coverage options.

Building insurance carried by property owners may not adequately protect residents from liability claims, particularly when disputes arise over whether damage resulted from tenant negligence, building defects, or normal wear and tear. Understanding what security deposits actually cover in sharehouses explains how insurance gaps can leave residents financially responsible for expensive repairs and replacements.

Legal Complexity in Multi-Tenant Situations

Legal disputes involving sharehouses often involve multiple parties with varying levels of responsibility, financial capability, and legal standing, creating complex litigation scenarios that can be expensive and time-consuming to resolve. Traditional landlord-tenant law assumes simpler relationships than those found in shared living arrangements, leading to legal uncertainty when problems arise.

Contract terms and legal obligations in sharehouses frequently lack the clarity and specificity needed to address complex liability scenarios, leaving residents vulnerable to interpretations that may not align with their expectations or understanding of their responsibilities. Understanding why contract terms are more important than advertised prices emphasizes the importance of understanding legal obligations before committing to shared living arrangements.

International residents face additional legal complexity due to visa restrictions, language barriers, and unfamiliarity with Japanese legal systems that can limit their ability to effectively navigate liability claims or legal disputes. Understanding why language barriers create more issues than expected illustrates how communication problems can escalate into serious legal and financial consequences.

Cross-cultural misunderstandings can contribute to liability situations when residents have different expectations about safety, responsibility, and appropriate responses to emergencies or accidents. These cultural differences can complicate legal proceedings and make resolution more difficult and expensive for all parties involved.

Financial Impact and Cost Multiplication

The financial consequences of liability incidents in sharehouses often exceed initial damage or injury costs due to the complex chain of effects that shared living arrangements can trigger. Legal fees, temporary accommodation costs, insurance deductibles, and lost security deposits can accumulate quickly when liability disputes involve multiple parties and extended resolution processes.

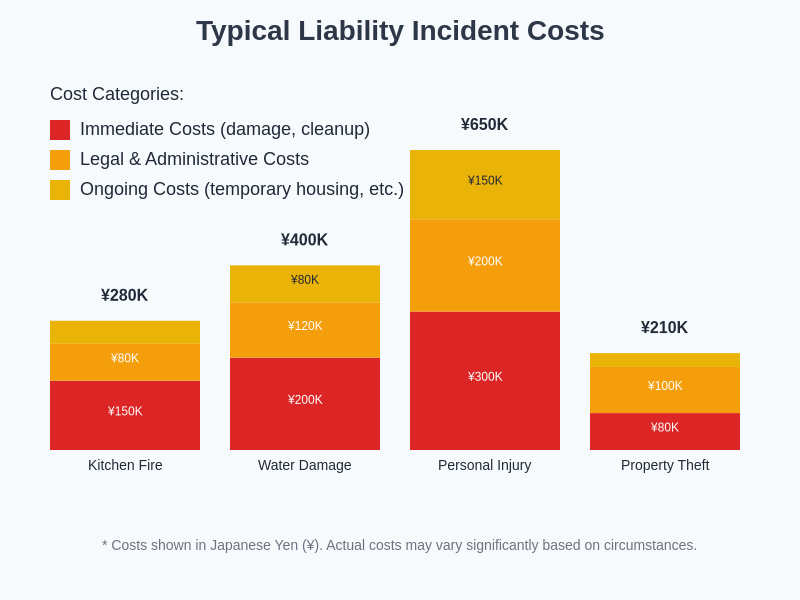

The cost analysis demonstrates how different types of liability incidents can escalate into substantial financial burdens, with personal injury claims representing the highest potential costs that can reach hundreds of thousands of yen when legal and ongoing expenses are factored into total incident costs.

Shared financial responsibility for common area damage or liability claims can create ongoing disputes among residents with different financial capabilities and willingness to pay, potentially leading to legal action and additional costs for all parties involved. Understanding how to budget realistically for sharehouse living includes considerations for unexpected liability expenses that residents should anticipate.

The reputation and credit implications of liability disputes can extend beyond immediate financial costs to affect future housing applications, employment opportunities, and financial standing in ways that may not be immediately apparent but can have long-term consequences for affected individuals.

Recovery of liability-related costs from responsible parties can be difficult or impossible when residents lack sufficient assets, leave the country, or dispute their responsibility, leaving other residents to absorb financial losses that they did not directly cause but cannot avoid due to shared living arrangements.

Risk Mitigation and Protection Strategies

Effective liability protection in sharehouses requires proactive strategies that address the unique risks of shared living while maintaining the social and economic benefits that attract residents to this housing model. Understanding and implementing appropriate protective measures can significantly reduce exposure while preserving positive living experiences.

Comprehensive personal liability insurance specifically designed for shared living situations provides essential protection against the elevated risks that standard renters insurance may not adequately cover. Working with insurance professionals who understand sharehouse living arrangements ensures that coverage matches actual exposure levels and risk scenarios.

Documentation practices become crucial for liability protection, including photographic records of room and common area conditions, written communication about safety concerns, and incident reports that can provide important evidence if disputes or claims arise. Understanding why written house rules get misinterpreted demonstrates the importance of clear documentation and communication in shared living environments.

Regular safety assessments and proactive communication about potential hazards can help prevent liability situations while creating documentation that demonstrates reasonable care and attention to shared living responsibilities. Understanding how to handle roommate conflicts without moving out includes strategies for addressing safety and liability concerns before they escalate into serious problems.

Emergency Response and Crisis Management

Emergency situations in sharehouses create heightened liability exposure due to the need for rapid response coordination among multiple residents who may have different emergency training, language abilities, and cultural approaches to crisis management. Effective emergency preparedness can significantly reduce liability risks while protecting resident safety and property.

Fire safety protocols become particularly important in shared living environments where cooking activities, electrical usage, and potential evacuation challenges can create scenarios where individual actions significantly impact other residents’ safety and property. Understanding why some buildings lack environmental features highlights infrastructure limitations that can complicate emergency response and increase liability exposure.

Medical emergency responses in sharehouses can create liability concerns when residents attempt to provide assistance, move injured parties, or make medical decisions that exceed their training or legal authority. Understanding appropriate boundaries and professional response protocols helps minimize liability while ensuring that injured residents receive proper care.

Natural disaster preparedness takes on additional complexity in sharehouses where evacuation procedures, emergency supplies, and communication protocols must account for multiple residents with varying preparedness levels and potential language barriers that could compromise response effectiveness and increase injury or property damage liability.

The shared living model fundamentally alters liability exposure through the interconnected nature of resident actions, property usage, and financial responsibility that traditional housing arrangements do not create. Understanding these elevated risks and implementing appropriate protective strategies enables residents to enjoy the benefits of communal living while minimizing their exposure to unexpected legal and financial consequences.

Successful sharehouse living requires recognition that personal liability extends beyond individual actions to encompass the complex web of relationships, responsibilities, and risks that emerge when multiple people share living spaces and facilities. Through careful attention to insurance coverage, documentation practices, safety protocols, and emergency preparedness, residents can protect themselves while contributing to positive and secure living environments for their entire sharehouse community.

Disclaimer

This article provides general information about personal liability in shared living spaces and should not be considered legal advice. Liability laws, insurance requirements, and tenant rights vary by jurisdiction and individual circumstances. Readers should consult with qualified legal and insurance professionals to understand their specific risks and protection options. The examples and scenarios presented are for educational purposes and may not reflect all possible liability situations or outcomes.