The harsh reality of sharehouse living in Tokyo reveals itself most painfully when residents discover that their security deposits, those substantial upfront payments they assumed would protect them from losses, offer absolutely no coverage for stolen belongings. This fundamental misunderstanding has left countless international residents financially devastated after experiencing theft, creating situations where victims face the dual trauma of losing valuable possessions and discovering they have no financial recourse through their housing arrangements.

The misconception that security deposits provide comprehensive protection stems from fundamental differences between housing systems across countries, language barriers in contract interpretation, and the complex legal framework governing rental agreements in Japan. Understanding these limitations becomes crucial for international residents who need to implement alternative protection strategies before experiencing the devastating financial impact of theft in shared living environments.

Understanding Security Deposit Fundamentals

Security deposits in Tokyo sharehouses serve exclusively as financial protection for property owners against tenant-caused damage to physical structures, furnishings, and fixtures within the rental property. The legal framework surrounding these deposits specifically excludes personal property protection, creating a clear distinction between property damage caused by tenants and losses resulting from criminal activity by third parties or other residents.

The standard security deposit amount, typically ranging from one to three months of rent, reflects the anticipated cost of repairing or replacing damaged property elements such as wall repairs, carpet cleaning, furniture restoration, and facility maintenance that exceeds normal wear and tear. What security deposits actually cover in sharehouses provides detailed explanations of specific coverage limitations that residents must understand before signing rental agreements.

Property management companies and sharehouse operators maintain strict policies regarding security deposit utilization, with detailed documentation requirements for any deductions and specific timelines for deposit return processes. These administrative procedures focus entirely on documenting property condition and calculating repair costs, with no mechanisms in place for addressing personal property theft or compensation claims.

The legal distinction between landlord liability for property maintenance and tenant responsibility for personal property protection creates fundamental gaps in coverage that many international residents fail to recognize until after experiencing losses. This separation of responsibilities reflects Japanese legal principles that place personal property protection squarely within individual tenant obligations rather than landlord or management company responsibilities.

Legal Limitations and Liability Boundaries

Japanese rental law establishes clear boundaries regarding landlord liability for tenant belongings, with specific legal precedents that consistently exempt property owners from responsibility for theft, burglary, or personal property damage caused by third parties. These legal protections for property owners stem from established principles that distinguish between providing safe habitable spaces and ensuring individual security for personal belongings.

The concept of reasonable care in Japanese housing law requires landlords to maintain basic security measures such as functioning locks, adequate lighting, and structural integrity, but does not extend to guaranteeing protection against criminal activity or providing compensation for theft losses. Legal disputes that get resolved in sharehouses illustrates how these liability limitations affect actual cases and dispute resolution outcomes.

International residents often discover these legal limitations only after filing police reports and attempting to seek compensation through their housing arrangements, creating situations where language barriers compound the already complex process of understanding Japanese legal protections and limitations. The cultural expectation that individuals take primary responsibility for protecting personal belongings reflects broader social values that emphasize personal accountability over institutional protection.

Contract language specifically excludes theft coverage through carefully worded clauses that may be difficult for non-native speakers to fully comprehend, particularly when combined with legal terminology that requires cultural context for proper interpretation. These contractual exclusions typically include comprehensive lists of scenarios where management companies bear no responsibility, with theft and burglary prominently featured among excluded circumstances.

Common Theft Scenarios in Sharehouses

The shared nature of sharehouse living creates numerous opportunities for theft that residents may not anticipate, particularly in environments where multiple individuals have varying levels of access to common areas and private spaces. Theft prevention that requires constant vigilance explores the practical realities of protecting belongings in communal living situations where traditional security measures prove inadequate.

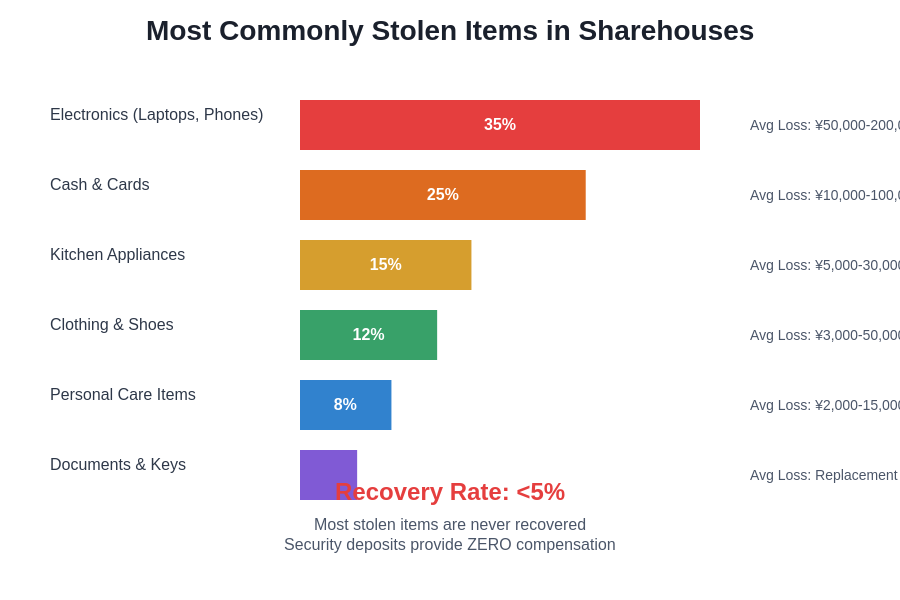

Electronics represent the most frequently stolen items in sharehouses, with laptops, smartphones, gaming systems, and cameras being particularly vulnerable due to their high resale value and easy portability. The international nature of many sharehouse residents creates situations where expensive electronics from different countries become attractive targets for opportunistic theft, especially during periods of high resident turnover or when security measures become lax.

Kitchen appliances and cooking equipment frequently disappear from common areas, creating situations where residents lose personal items they brought to enhance shared facilities. The ambiguous nature of ownership for items placed in common areas creates opportunities for both accidental appropriation and deliberate theft, with limited recourse available for recovering stolen cooking equipment or appliances.

Personal clothing, shoes, and accessories often vanish from laundry areas, bathrooms, and entryways where residents store personal items in shared spaces. The cultural differences regarding personal space and property boundaries can contribute to situations where theft occurs under the guise of borrowing or mistaken ownership, particularly when language barriers prevent clear communication about ownership expectations.

Cash and important documents become particularly vulnerable in sharehouse environments where private room security may be compromised by key sharing, inadequate locks, or unauthorized access during cleaning or maintenance activities. Personal belongings that disappear despite locks examines how even seemingly secure storage solutions fail to prevent determined theft in shared living environments.

Financial Impact and Recovery Challenges

The financial devastation experienced by theft victims extends far beyond the immediate value of stolen items, encompassing replacement costs, time lost dealing with aftermath, and the emotional toll of violated security in what should be a safe living environment. International residents face particular challenges when attempting to recover from theft, as replacement items may require international shipping, specialized sourcing, or currency conversion that significantly increases actual replacement costs.

Insurance complications arise when residents discover that standard renter’s insurance policies may not provide adequate coverage for items stolen from shared living situations, particularly when policy language excludes coverage for property theft in commercial or semi-commercial housing arrangements. Living in sharehouses affects your insurance coverage reveals how residence type can impact insurance eligibility and coverage options available to international residents.

The replacement value of stolen electronics, particularly items purchased in other countries, often exceeds the cost of similar items available in Japan due to import costs, model availability, and currency exchange fluctuations. Specialized equipment, professional tools, and personal items with sentimental value may prove impossible to replace, creating losses that extend beyond monetary considerations into personal and professional impact areas.

Documentation challenges complicate insurance claims and police reports when residents lack purchase receipts, serial numbers, or photographic evidence of stolen items. The international nature of many possessions creates additional complexity when attempting to establish ownership, value, and replacement costs for items originally purchased in other countries using different currencies and through different retail systems.

Alternative Protection Strategies

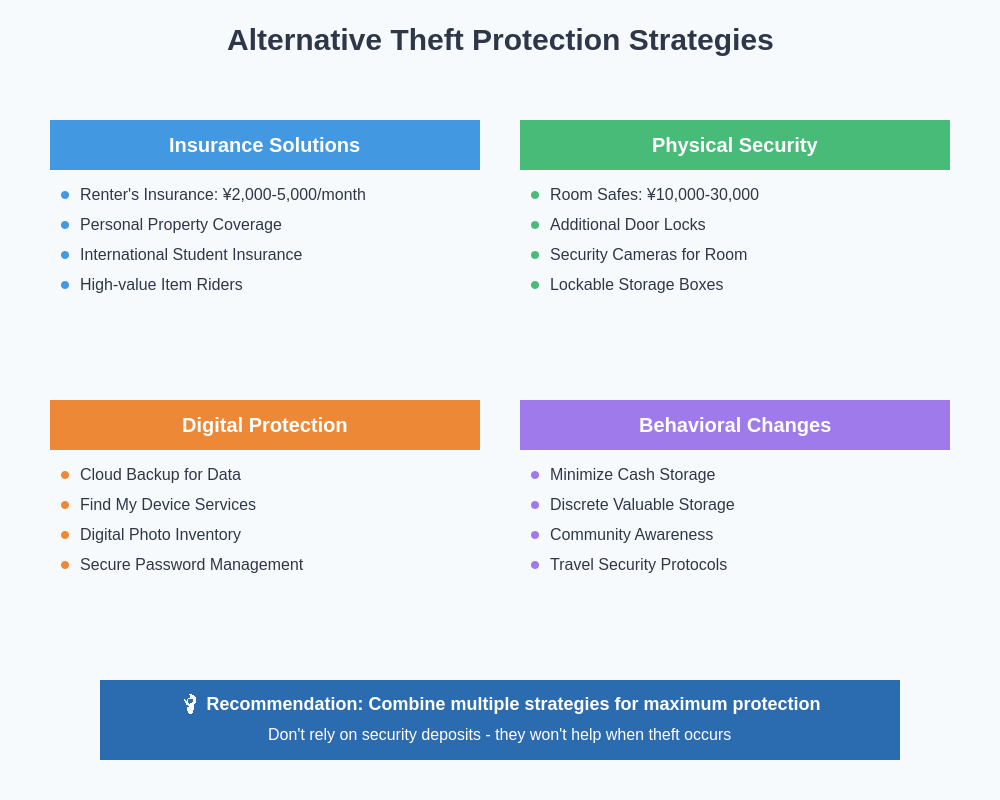

Personal insurance solutions provide the most reliable protection against theft losses in sharehouse environments, with renter’s insurance policies specifically designed to cover personal property regardless of housing type or theft location. International residents must carefully evaluate insurance options to ensure coverage extends to their specific living situation and includes adequate protection for high-value electronics and personal belongings.

Secure storage solutions within private rooms become essential for protecting valuable items, with lockable cabinets, safes, and discrete storage systems providing better protection than relying on room locks alone. How smart locks change sharehouse security explores technological solutions that can enhance personal security within shared living environments.

Documentation and inventory management help residents maintain records of valuable possessions, including serial numbers, purchase receipts, and photographic evidence that supports insurance claims and police reports in case of theft. Creating digital backups of important documents and maintaining updated inventory lists provides crucial evidence for recovering losses through insurance claims or legal proceedings.

Community awareness and communication strategies can reduce theft opportunities by establishing clear expectations regarding personal property, implementing informal monitoring systems, and creating social pressure that discourages opportunistic theft among residents. Building real friendships takes longer than expected examines how developing genuine relationships with housemates can contribute to community security and mutual protection.

Banking and financial protection measures include minimizing cash storage in sharehouse rooms, utilizing secure digital payment methods, and maintaining financial accounts that provide fraud protection and transaction monitoring. International residents should establish banking relationships that offer comprehensive protection against unauthorized access and provide rapid response to suspicious activity.

Insurance Options and Coverage Gaps

Renter’s insurance policies available to international residents in Japan vary significantly in terms of coverage scope, premium costs, and eligibility requirements that may exclude certain visa categories or temporary residents. Understanding policy limitations becomes crucial for residents who need comprehensive protection against theft while living in shared housing arrangements that may not qualify for standard residential coverage.

International insurance policies offered through home country providers may provide broader coverage but can create complications regarding claim processing, currency conversion, and policy enforcement within Japanese legal frameworks. How international money transfers cost more explores the financial complexities that affect international insurance arrangements and claim settlements.

Specialized insurance products designed for temporary residents and international students often provide better alignment with sharehouse living situations, offering coverage that accounts for the unique risks and challenges associated with communal living arrangements. These policies may include provisions for theft in shared spaces, temporary accommodation coverage, and protection for high-value electronics commonly owned by international residents.

Coverage gaps commonly occur in areas such as theft from common areas, items stolen by other residents, and losses that occur during temporary travel or extended absences from the sharehouse. Understanding these limitations helps residents make informed decisions about additional coverage needs and alternative protection strategies for items that fall outside standard policy coverage.

Practical Prevention Measures

Physical security measures within private rooms include installing additional locks, using portable safes, and implementing discrete storage solutions that make theft more difficult and time-consuming. The effectiveness of these measures depends on consistent implementation and selecting security solutions appropriate for the specific room layout and access patterns within the sharehouse.

Behavioral strategies reduce theft opportunities by maintaining awareness of surroundings, limiting discussions about valuable possessions, and avoiding displays of expensive electronics or cash that might attract unwanted attention from other residents or visitors. Social hierarchies that develop naturally examines how community dynamics can either contribute to or prevent theft opportunities within sharehouse environments.

Technology solutions such as security cameras for private rooms, tracking devices for valuable electronics, and digital monitoring systems can provide evidence in case of theft while potentially deterring opportunistic criminals. However, residents must balance security needs with privacy considerations and house rules that may restrict surveillance equipment in shared spaces.

Community engagement and relationship building create informal security networks where residents look out for each other’s property and report suspicious activity. Making friends through Tokyo sharehouse communities explores how developing genuine relationships with housemates can contribute to mutual security and reduce theft opportunities through increased community awareness.

Legal Recourse and Recovery Options

Police reporting procedures for theft in sharehouses involve specific documentation requirements and investigative processes that may differ from theft reports in other housing situations. International residents must understand their rights and responsibilities when filing reports, including language support options and cultural expectations regarding cooperation with law enforcement investigations.

Civil legal action against other residents suspected of theft faces significant challenges including evidence requirements, language barriers, and the temporary nature of many sharehouse residents who may leave before legal proceedings conclude. Legal disputes that get resolved in sharehouses provides insights into the practical limitations of pursuing legal remedies for theft in shared living situations.

Management company obligations regarding theft incidents typically focus on cooperation with law enforcement and implementing reasonable security measures, but rarely extend to financial compensation or extensive investigative efforts. Understanding these limitations helps residents set appropriate expectations regarding support available from housing operators after experiencing theft.

Recovery through insurance claims provides the most reliable path for financial recovery, but requires proper documentation, timely reporting, and policy coverage that specifically includes theft protection for personal property in shared living situations. The claim process can be complex for international residents, particularly when dealing with Japanese insurance companies and language barriers that affect communication.

Long-term Security Planning

Risk assessment for different sharehouse types reveals that certain housing arrangements present higher theft risks due to factors such as resident turnover rates, security infrastructure quality, and management company policies regarding access control and incident response. Security cameras that create false sense of safety examines how apparent security measures may not provide actual protection against determined theft.

Budget planning for security measures and insurance coverage should account for ongoing costs such as insurance premiums, secure storage solutions, and replacement reserves that provide financial cushioning in case of significant theft losses. These security investments represent essential expenses rather than optional conveniences for residents living in shared housing environments.

Transition planning for residents who experience significant theft may include considerations for relocating to more secure housing, upgrading security measures in current arrangements, or modifying lifestyle patterns to reduce theft vulnerability. The psychological impact of theft often necessitates changes beyond simple property replacement, affecting residents’ sense of security and comfort in shared living situations.

Community involvement in security improvements can create positive changes that benefit all residents, including advocating for better locks, improved lighting, enhanced access controls, and clearer security policies from management companies. How house rules get misinterpreted explores how residents can work together to establish clearer security expectations and preventive measures.

The reality that security deposits provide no protection against theft represents a fundamental aspect of sharehouse living that international residents must understand and prepare for through alternative protection strategies. By implementing comprehensive security measures, maintaining appropriate insurance coverage, and developing community awareness, residents can protect themselves against the financial and emotional impact of theft while enjoying the benefits of shared living in Tokyo’s dynamic housing market.

Disclaimer

This article is for informational purposes only and does not constitute legal or insurance advice. Security deposit terms, insurance coverage, and legal remedies may vary significantly between different sharehouses and insurance providers. Readers should carefully review their specific contracts and consult with qualified professionals regarding insurance needs and legal options. The effectiveness of security measures and prevention strategies may vary depending on individual circumstances and specific sharehouse environments.