The stark reality of sharehouse living in Tokyo extends far beyond the monthly rent payments and social dynamics that most residents focus on when selecting their accommodation. Insurance protection represents one of the most overlooked yet potentially devastating aspects of shared living arrangements, with thousands of international residents discovering annually that their assumptions about coverage can lead to financial ruin when unexpected incidents occur. The complexity of Japanese insurance systems, combined with the unique risks inherent in shared living environments, creates a perfect storm of vulnerability that can destroy personal finances and derail life plans without proper preparation and understanding.

The misconceptions surrounding insurance coverage in sharehouses stem largely from cultural differences in how insurance systems operate across different countries, leading many international residents to assume that basic coverage extends to scenarios that are explicitly excluded from standard policies. Understanding the true scope of insurance protection becomes particularly crucial when considering the financial implications of common sharehouse incidents that can result in liability claims ranging from thousands to millions of yen, potentially affecting residents for years or even decades after the initial incident occurs.

The Hidden Vulnerabilities of Shared Living Spaces

Sharehouse environments create unique risk profiles that differ dramatically from traditional apartment living, exposing residents to liability scenarios that rarely occur in single-occupancy housing situations. The presence of multiple residents with varying levels of responsibility, different cultural backgrounds regarding property care, and diverse lifestyle habits creates exponential increases in potential accident scenarios that can trigger insurance claims and liability disputes.

Kitchen fires represent one of the most common yet devastating risks in sharehouse environments, where multiple residents with different cooking experiences and cultural food preparation methods share the same facilities throughout extended periods. Understanding utility bills in Japanese sharehouses often reveals how shared responsibility can lead to confusion about who bears liability when accidents occur due to equipment misuse or maintenance neglect.

The interconnected nature of sharehouse systems means that individual actions can have cascading effects throughout the entire building, turning minor incidents into major disasters that affect multiple residents and potentially the broader building community. Water damage from overflowing bathtubs or washing machines can destroy personal belongings belonging to residents on lower floors, creating complex liability chains that standard insurance policies may not adequately address without specific shared living endorsements.

Personal property theft in sharehouses presents particularly complex insurance challenges due to the difficulty of establishing clear boundaries between communal and private spaces, and the challenge of proving theft versus misplacement in environments where multiple people have varying levels of access to different areas. The social dynamics that make sharehouses attractive for community building can simultaneously create opportunities for internal theft that traditional insurance policies struggle to address effectively.

These common risk scenarios demonstrate the wide range of potential incidents that can occur in sharehouse environments, each with significant financial implications for unprepared residents. Understanding both the probability and potential cost of each scenario helps residents make informed decisions about appropriate insurance coverage levels.

Understanding Japanese Insurance System Complexities

The Japanese insurance landscape operates under fundamentally different principles than many Western insurance systems, with distinctions between coverage types, liability assignments, and claim procedures that can confuse international residents accustomed to different insurance paradigms. Renter’s insurance in Japan typically provides more limited coverage than comparable policies in other countries, while simultaneously imposing stricter requirements for policy maintenance and claim documentation that can void coverage if not properly managed.

Liability insurance becomes particularly complex in sharehouse situations where the distinction between individual responsibility and collective responsibility often remains unclear until an incident occurs and insurance companies begin investigating fault assignments. What security deposits actually cover in sharehouses frequently excludes major damage scenarios that residents assume would be covered, leaving significant gaps that require separate insurance protection to address adequately.

The concept of “key money” and various deposit structures in Japanese rental agreements can create false impressions about insurance coverage, leading residents to believe that these upfront payments provide broader protection than they actually offer. Many sharehouse operators maintain building insurance that protects their interests as property owners but provides minimal or no protection for resident belongings or resident liability exposure, requiring individual residents to secure their own comprehensive coverage.

Language barriers significantly complicate insurance navigation for international residents, with policy documents, claim procedures, and coverage explanations often available only in Japanese or requiring cultural context that may not be immediately apparent to foreign residents. The technical terminology used in Japanese insurance policies can be particularly challenging to understand, even for residents with functional Japanese language skills, leading to misunderstandings about coverage scope and claim requirements.

The Real Cost of Inadequate Coverage

Financial devastation from inadequate insurance coverage in sharehouses can extend far beyond the immediate costs of replacing damaged belongings or paying for property repairs, creating long-term financial obligations that can affect residents for years after they leave their sharehouse accommodations. Liability claims from accidents that injure other residents or damage building systems can result in court judgments that require payment plans extending over multiple years, significantly impacting future financial planning and life goals.

Medical expenses resulting from accidents in sharehouses can accumulate rapidly in Japan’s healthcare system, particularly for residents without comprehensive health insurance or those whose conditions require specialized treatments not covered by basic national health insurance. Living costs in Tokyo sharehouses explained rarely account for the potential emergency expenses that can arise from inadequate insurance protection, leaving residents financially vulnerable when accidents occur.

The replacement costs for personal belongings destroyed in sharehouse incidents often exceed residents’ expectations, particularly for electronics, clothing, and specialized items that may be more expensive to replace in Japan than in residents’ home countries. International shipping costs, import duties, and the time required to replace essential items can create additional financial burdens beyond the direct replacement costs, especially for residents who rely on specific equipment for work or study purposes.

Professional liability exposure represents an often-overlooked risk for residents who work from their sharehouse accommodations, as accidents or damages that interfere with work responsibilities can trigger additional liability claims from employers or clients who suffer losses due to the resident’s inability to fulfill professional obligations. Real stories from Tokyo sharehouse residents frequently include examples of career disruptions caused by inadequately insured incidents.

Navigating Insurance Options and Requirements

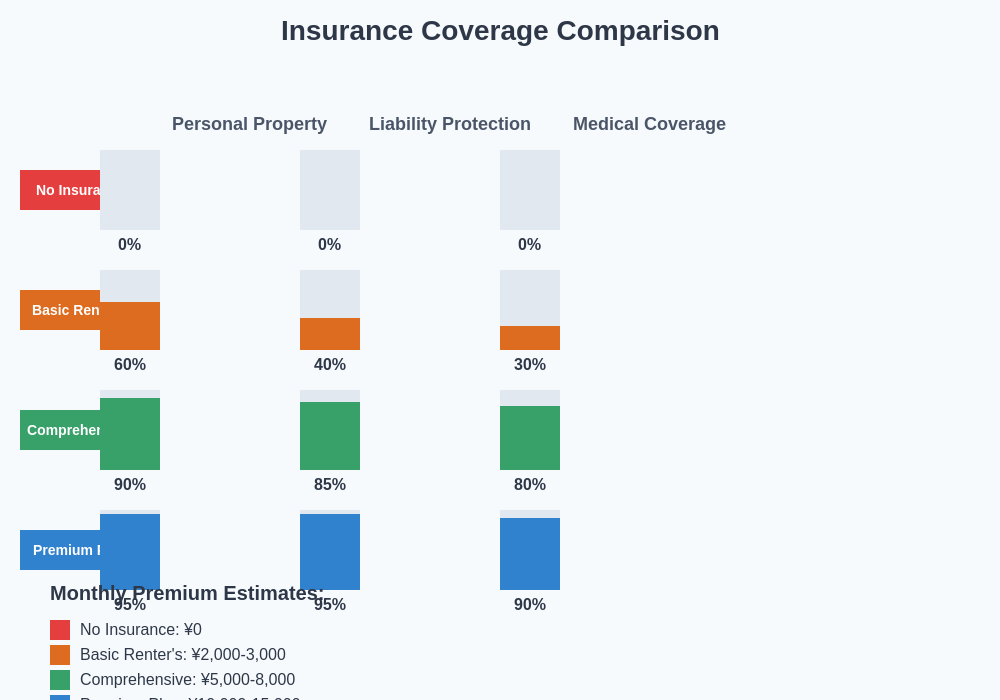

The landscape of available insurance options for sharehouse residents encompasses multiple policy types and coverage combinations that require careful evaluation to ensure comprehensive protection without unnecessary duplication or gaps in coverage. Personal property insurance, liability insurance, and specialized renter’s insurance each address different risk categories, but understanding how these policies interact and where coverage gaps might exist requires detailed analysis of policy terms and conditions.

Comprehensive renter’s insurance represents the foundation of protection for most sharehouse residents, providing coverage for personal belongings and basic liability protection, but the specific terms and exclusions of these policies can vary dramatically between insurance providers and policy levels. The cost-benefit analysis of different coverage levels must account for the unique risks of sharehouse living while balancing premium costs against potential exposure levels.

Additional liability coverage beyond basic renter’s insurance becomes particularly important for residents whose activities, possessions, or lifestyle choices create elevated risk profiles that exceed standard policy limits. Japanese sharehouse rules every foreigner should know often include requirements or recommendations for specific insurance coverage levels that residents should maintain to comply with house policies and protect themselves adequately.

International residents face additional complexity in determining whether existing insurance policies from their home countries provide any coverage for incidents occurring in Japan, and whether maintaining home country policies alongside Japanese coverage creates beneficial overlap or problematic duplication that could complicate claim processing. The coordination of benefits between multiple insurance policies requires careful documentation and understanding of how different insurance systems interact across international boundaries.

This comparison illustrates the dramatic differences in protection levels between various insurance options available to sharehouse residents. The gap between basic coverage and comprehensive protection can mean the difference between minor inconvenience and financial disaster when incidents occur.

Specific Risks in Tokyo Sharehouse Environments

Tokyo’s unique urban environment creates specific risk factors that may not exist in other cities or countries, requiring insurance considerations tailored to local conditions and potential scenarios that residents might not anticipate based on their previous living experiences. Earthquake and natural disaster coverage becomes particularly crucial given Japan’s seismic activity, but standard renter’s insurance may exclude or limit coverage for earthquake-related damages unless specific endorsements are purchased.

The density of Tokyo’s housing market and the age of many buildings used for sharehouses create elevated risks for structural issues, electrical problems, and plumbing failures that can cause damage extending beyond individual rooms to affect multiple residents and common areas. Best sharehouses in Tokyo often feature older buildings that have been converted for shared living, potentially creating insurance challenges related to building age and modification history.

Transportation-related risks specific to Tokyo’s extensive rail system can affect sharehouse residents through delayed or cancelled commutes that interfere with work obligations, but travel delay insurance and related coverage options may not be readily apparent to international residents unfamiliar with Japanese insurance market offerings. The interconnected nature of Tokyo’s transportation system means that disruptions can have cascading effects on resident schedules and obligations.

Bicycle theft and damage represent particularly common risks for sharehouse residents who rely on cycling for daily transportation, but coverage for bicycles under standard renter’s insurance policies may be limited or subject to specific security requirements that residents must understand and maintain to ensure coverage validity. The high cost of quality bicycles in Japan makes adequate insurance protection particularly important for residents who depend on cycling for regular transportation.

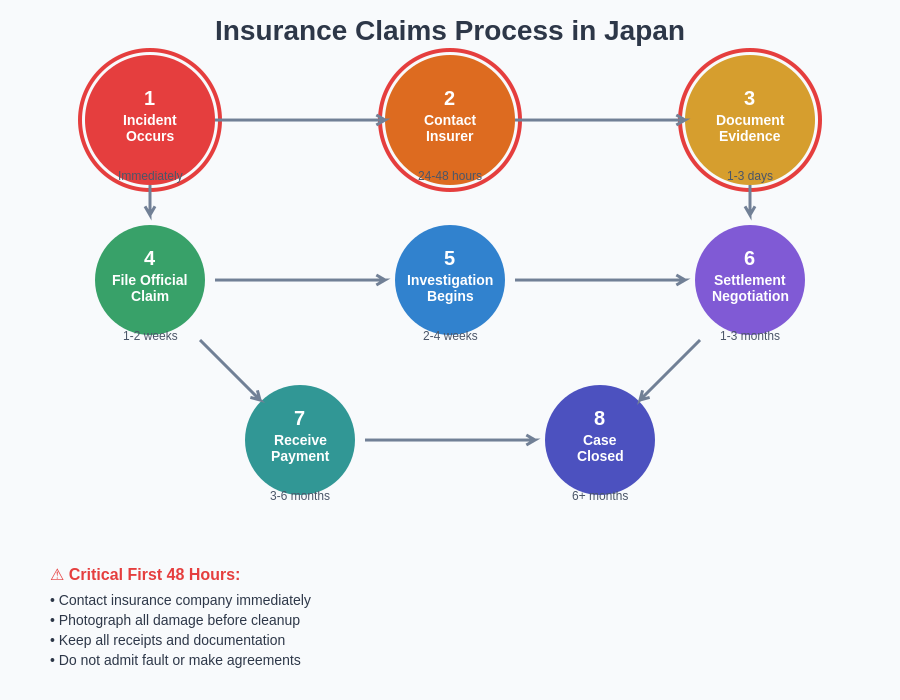

The Application and Claims Process Reality

Understanding the practical realities of insurance application and claims processes becomes crucial for residents who want to ensure their coverage will function effectively when needed, rather than discovering limitations or complications after incidents have already occurred. The documentation requirements for insurance applications in Japan often exceed what international residents expect, requiring specific forms of identification, address verification, and financial documentation that may be challenging to obtain during the initial settling-in period.

Claims processing procedures in Japanese insurance systems typically involve more detailed investigation and documentation requirements than many international residents anticipate, with specific procedures for reporting incidents, preserving evidence, and coordinating with other parties that must be followed precisely to avoid claim denial or reduced settlements. The timeline for claims resolution can extend significantly longer than residents expect, particularly for complex incidents involving multiple parties or significant damages.

Language support for claims processing varies dramatically between insurance providers, with some offering comprehensive English-language support while others require Japanese language proficiency or professional translation services that can add complexity and cost to the claims process. What moving out really costs in Tokyo sharehouses sometimes includes unexpected insurance-related expenses when claims processes extend beyond residents’ planned departure dates.

The coordination between sharehouse management, building ownership, and individual residents during claims processing can create complex communication chains that require careful management to ensure all parties receive necessary information and documentation. Understanding each party’s responsibilities and communication protocols before incidents occur helps streamline claims processing and reduces the likelihood of delays or complications.

The insurance claims process in Japan follows a specific timeline and requires immediate action during the first 48 hours after an incident occurs. Understanding this process before an emergency helps ensure proper procedures are followed and claims are processed efficiently.

Prevention Strategies and Risk Management

Proactive risk management strategies can significantly reduce the likelihood of incidents that trigger insurance claims while simultaneously demonstrating responsible behavior that can positively influence insurance pricing and claims processing outcomes. Understanding how insurance companies evaluate risk factors in sharehouse environments enables residents to make informed decisions about their behavior and property management that can reduce both premiums and claim likelihood.

Regular maintenance awareness and reporting procedures help identify potential problems before they escalate into major incidents that could affect multiple residents or result in significant damages. How to find the perfect sharehouse in Tokyo should include evaluation of building maintenance standards and management responsiveness, as these factors directly influence insurance risk profiles and coverage requirements.

Personal property protection strategies extend beyond insurance coverage to include security measures, storage protocols, and documentation practices that can prevent losses and facilitate claims processing when incidents do occur. Maintaining detailed inventories of personal belongings, including photographs and purchase receipts, creates essential documentation for insurance claims while helping residents understand the true value of their possessions and appropriate coverage levels.

Community communication and incident reporting protocols help ensure that all residents understand their responsibilities for maintaining safe living conditions and reporting potential problems before they escalate into insurance-claiming events. Building positive relationships with sharehouse management and fellow residents creates support networks that can assist with problem resolution and emergency response when incidents occur.

Long-term Financial Planning Considerations

Insurance costs represent ongoing financial obligations that should be integrated into long-term budgeting and financial planning for sharehouse residents, particularly those planning extended stays in Tokyo or those considering transitions to other housing arrangements. The cumulative cost of comprehensive insurance protection over multiple years must be balanced against the potential financial devastation that could result from inadequate coverage during a single major incident.

Understanding how insurance history and claims experience can affect future insurance availability and pricing helps residents make informed decisions about claim filing and risk management throughout their residency period. Maintaining continuous insurance coverage and a clean claims history can provide advantages when transitioning between different housing arrangements or when adjusting coverage levels to match changing circumstances.

The relationship between insurance coverage and other financial planning elements, including emergency fund requirements, investment strategies, and career planning, requires integrated consideration to ensure that insurance decisions support overall financial goals while providing adequate protection. Insurance should complement rather than replace other financial protection strategies, working together to create comprehensive financial security.

International considerations become particularly important for residents planning to return to their home countries or relocate to other international destinations, as insurance claims history and coverage gaps can affect future insurance availability and pricing in different countries. Understanding how Japanese insurance experience translates to insurance applications in other countries helps residents make informed decisions about coverage levels and claims management.

The evolving nature of sharehouse living in Tokyo, including changes in regulations, building standards, and insurance market offerings, requires ongoing attention to ensure that insurance coverage remains adequate and current with changing circumstances. Regular review and adjustment of insurance coverage helps ensure continued protection as residents’ circumstances change and as the broader sharehouse market evolves.

Insurance protection in Tokyo sharehouses represents far more than a simple financial transaction or regulatory requirement, functioning instead as a critical foundation for financial security and peace of mind that enables residents to fully engage with the opportunities and experiences that sharehouse living provides. The investment in comprehensive insurance coverage pays dividends not only through direct financial protection but also through the confidence and security that allow residents to focus on their personal and professional goals rather than worrying about potential financial disasters.

Disclaimer

This article is for informational purposes only and does not constitute professional insurance or legal advice. Insurance requirements, coverage options, and regulations in Japan may change, and individual circumstances vary significantly. Readers should consult with qualified insurance professionals and carefully review all policy documents before making insurance decisions. The effectiveness of insurance strategies mentioned may vary depending on specific circumstances, policy terms, and insurance company practices.